Is mutual funds taxation different in case of NRIs? Is not the capital gain tax on mutual funds for Non-residents same as of resident Indians?

The answer is both Yes & NO.

This is a common understanding that the Non-residents are treated at par with Residents in case of Mutual fund investments. But actually, this is not the case.

Then how is it different for NRIs? This is the question which today we will find the answer of. But before looking at how it is different, we first try to understand how mutual funds taxation actually works

(Read: Who is an NRI – as per Income tax and FEMA laws)

Mutual Funds Taxation – Factors to consider

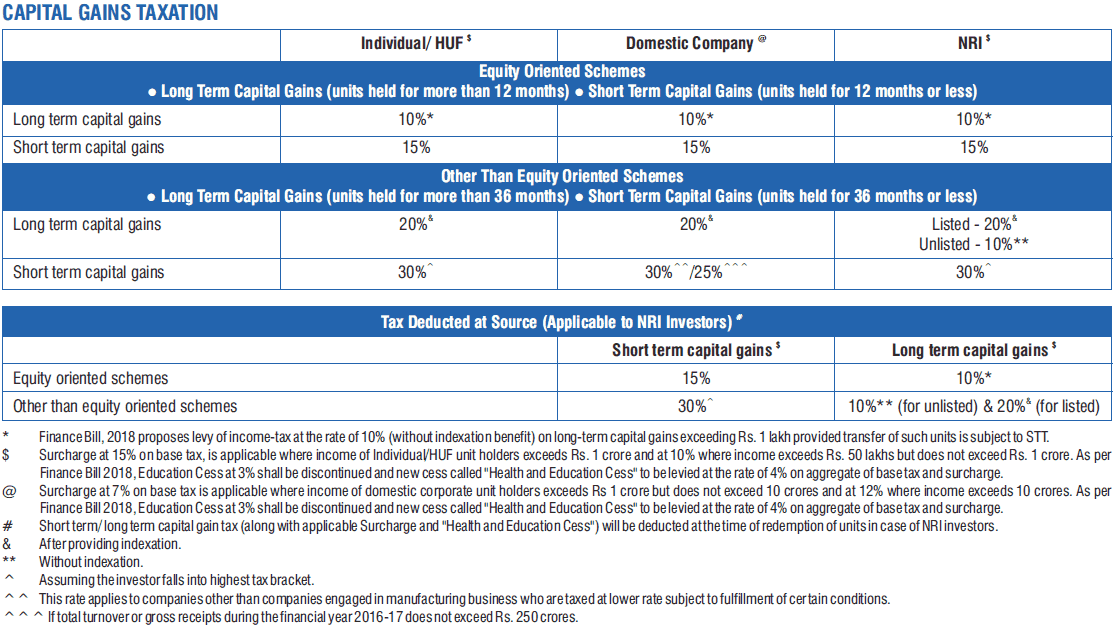

Capital gain tax on mutual funds depends on 2 major factors – Type of fund and the holding period of the investments.

Broadly there are 2 types of funds if we look at it from taxation angle:

Equity and Non-Equity

Equity funds are those funds where the composition of equity and equity related instruments in the portfolio is 65% and above.

Non-Equity funds are all those funds which do not satisfy the above-mentioned condition. Means all categories of Debt mutual funds, Hybrid funds with less than 65% equity exposure, Gold funds etc all are Non-Equity funds.

Besides the Type of fund, the Holding period of the scheme in your portfolio, also determines Mutual funds taxation. Based on Holding period there are 2 segments in capital gain taxation.

Long-term and Short-term.

In case of Equity mutual funds, if the holding period is more than 1 year, then it falls under Long-term capital gain taxation otherwise it remains short term. Whereas,

In Non-Equity Mutual funds, if the holding period is more than 3 years, then it falls under Long-term capital gain taxation otherwise it remains short term.

Capital Gains Tax on Mutual funds – Tax rates

The below table shows the rate of capital gains tax in case of different holding periods and also the type of funds.

Mutual funds taxation – How is it different for Non-Residents?

Residential status also impacts the capital gains tax on mutual funds. Yes, commonly it is known that capital gains tax on mutual funds works same with Residents and Non-residents. But that is not completely true.

While Long-term capital gains tax in case of equity fund both Residents and non-residents have to pay 10% (w.e.f. 01.04.2018), in the case of Non-Equity funds the rules are different.

NRIs are not allowed to take Indexation benefit in case of Unlisted debt Securities.

As per Income tax rules, in the case of Long-term capital gains in Non-Equity schemes, NRIs are subject to 20% tax rate after Indexation in case of Listed schemes; and 10% without Indexation in case of Unlisted schemes. (Read: What is indexation and how to calculate Indexed cost of acquisition?)

So, if we take a look at the listing status of different mutual fund schemes, then only Close-ended schemes get mandatorily listed on stock exchange and Rest all Open-ended schemes remain unlisted.

This means that if an NRI books a Long-term capital gain from a Non-Equity Mutual fund which is not listed on the stock exchange then he/she will have to pay 10% of the gains as capital gains tax, whereas if the scheme is listed on the exchange (like a Fixed Maturity Plan) then the tax rate would be 20% after adjusting for indexation.

This is not all, unlike Residents, in the case of capital gains tax on mutual funds NRIs are subject to TDS on the Capital gains. In fact, not only in mutual funds, NRIs are subject to TDS in almost all the investments they make in India.

Conclusion:

It is always important to be on the right side of the law. Sometimes what is commonly known may not be true and Ignorance can never be an excuse in legal issues.

The advantage with NRIs in case of Mutual funds taxation is the TDS which gets deducted at applicable tax rates. This may be construed as a disadvantage too when you do not have any other income in India.

That is why being aware of the tax laws is important so you should pay only what you are liable to and claim the refund of what has been deducted extra from your Income.

Hope you find the article on Capital gains tax on mutual funds useful. You may ask your queries if any in the comments section below.

Manikaran Singal is the founder and Chief financial planner at Good Moneying Financial Solutions. He is a CERTIFIED FINANCIAL PLANNER CM and SEBI registered Investment adviser (Regd no. INA 100001620). He’s having 20+ years of experience in financial services space.

Manikaran Singal is the founder and Chief financial planner at Good Moneying Financial Solutions. He is a CERTIFIED FINANCIAL PLANNER CM and SEBI registered Investment adviser (Regd no. INA 100001620). He’s having 20+ years of experience in financial services space.")

{kind=link}

Good article. I am an NRI and I understand that STCG on debt mutual funds is at applicable tax rates and also STCG on debt MFs is added to overall income for taxation purposes. Does that mean I can recover the 30% TDS via filing tax return ( if I fall in the lower tax bracket overall) and is that true for both NRE/ NRO Debt MF investments? Please help clarify. What is the treatment of LTCG for NRIs and are they added to overall income while filing return?

Yes, Anand. You may file ITR and claim a refund on the TDS deducted on STCG on debt funds. and yes it is true for both NRE and NRO accounts.

In the case of LTCG, the provisions are different for NRIs and you will not be able to claim the benefit of basic tax exemption limit and are supposed to pay tax on the gains booked.

Hi Mani,

Thank you for creating a nice informative page. Can you confirm if my understanding is correct, for the below taxation for NRIs.

Let us say I am an NRI. I have Rs 490,000 as STCG from debt funds in an year and no other income.

1. Can I use both Basic Exemption Limit and 80c deduction for this gain? (Since STCG in debt funds is not covered under section 111a).

2. For FY2018-2019, can I use the standard deduction of 40000?

3. Am I eligible for tax rebate till 300000?

In summary, I can show taxable income as (300000 = 490000-150000(80c)-40000(std deduction)) and hence will not pay any tax?

Thanks,

BR

Hi Roy

I am glad you like my article. Please find my replies to your query point by point

1. Yes for Basic exemption (only in case of STCG) and No for 80 C savings.

2. No. The standard deduction applies only in case of Salary Income.

3. If you are above 60 years of age…the YES.

This is as per my understanding of tax laws and I am not a tax expert. So please do clarify the same from a tax professional.

hi Manikaran – thanks for your reply and clarification. Truly appreciate you taking time to answer the questions I had.

Thanks, Anand. I am glad i was helpful.

Thank you for creating a nice informative page for NRI

I I invest in tax free fund like ELSS, I can save tax also if I use STP method to invest in SIP what will be the Tax procedure.

Sorry, Suneesh. Don’t get your query completely. Could you Please elaborate?

Hi, I don’t agree with the last point u made in this article ‘ In fact, not only in mutual funds, NRIs are subject to TDS in almost all the investments they make in India’. What about the fixed deposit? The NRI fds don’t attract TDS.

Yes, NRE FDs don’t attract any TDS

WHAT IS THE POSITION ON THE INVESTMENTS IN MUTUAL FUNDS BEFORE GOING ABROAD, ON INCOME I HAVE ALREADY PAID MY TAXES.THOSE INVESTMENTS ARE STILL CONTINUING.WHAT SHOULD I DO WITH THEM

THANKS.

If you want to continue your mutual fund investments in India, then you would have to convert your saving bank a/c to NRO account, so that whenever you redeem those investments, money should come in that account, and update your KYC. However, the decision to continue depends on your financial plan and goals you have in mind.

Wheth the AMC will give the capital gains of the fund redeemed equity,liquid Every thing

I assume that you are asking about capital gains Report. Yes the AMC would provide the same, but you have to ask for it.

i am an indian staying in Mumbai.My son whose in USA is working ther under OPT after his studies.He wants in invest some money in mf can he do that

Yes he can do so if he is aware of the taxation on mutual funds in USA. USA taxes global income. Also, there is point in investing in mutual funds in India only if he has plans to come back to India for good in future and use that money in India itself. Otherwise, he may go for offshore funds, which invest in India also.

I read in the article, LTCG is tax free, but i was charged 10.4% tds on long term hybrid fund on 24th October.

Why is it so? .i am an NRI

What is the threshold level , above which LTCG tds can be deducted for NRI customer

It seems you are being mistaken, we have mentioned the tax rate on equity oriented Mutual Funds as 10.4% for NRIs in our article and there is no threshold limit for the same for NRIs.

I am an NRI. I want to know about taxes i need to pay for my Mutual fund returns in India

what is the tax % applicable & how its deducted?

Please read the article below, wherein we have mentioned in detail the taxation of Mutual Funds for NRIs, still if you are left with any queries, feel free to mention it in comments.

https://www.goodmoneying.com/mutual-funds-taxation-nris/

Since ltcg on equities is fully deducted at source at 10 percent for an nri then does an nri need to file an income tax return if this is his only income?

Additional Query:

I am an NRI. Suppose Rs 40000 has been deducted as TDS from me and my taxable income in india is below basic tax-exemption limit. Can I claim back this TDS ? under which rule ?

I have ltcg of 1.95 lacs which is calculated at 10%. For an NRI do I need to pay tds of 10% on this or will the total 1.95 lacs be deducted as tds

We assume you are talking about Equity mutual fund long term capital gain, and in this case for NRIs, TDS gets deducted at the company level only. and will be on the Gain portion, not on the full amount.