These days you must be reading a lot in different media publications that the era of low-interest rates is soon going to be over and very soon you will see interest rates start rising from current levels.

All this has led to coming up with varied pieces of advice on what should bond market investors or debt mutual funds investor do look at the market scenario.

Because there is an inverse relationship between interest rates/yield and bond prices. When interest rate rises bond prices fall and when interest rates fall bond prices go up.

That is why long-term bond or debt mutual funds investors earn well in the falling rate scenario as experienced in 2015-16 when we saw 3 rate cuts in REPO by RBI.

Whereas in 2017 we saw quite a dim performance as RBI did not do any rate cut as markets were expecting post demonetization.

The Idea of this article is not to figure out where the interest rates are heading, and neither on what would be the RBI move in the next meet, but to give investors a clear picture on where should they invest their money in such kind of volatile interest rate scenario or in general, since just like equity market movements it is difficult to predict the debt market movements too.

There are many domestic and international factors that impact both, so its wise to have a clear strategy in place rather than just ruining the portfolio due to sentiments and media news.

Before moving ahead, let me give you a brief on what determines the interest rates in the Market.

The Interest rates are generally the factors of demand and supply of money. Demand by the borrowers and supply by the Banking system and other modes.

When demand is high, means borrowers are asking for more money, which may be due to better economic conditions, this further leads to increase in rates. Whereas when demand is low then banking wants to lend more so to increase the economic activities, and thus lower the rates.

The government of India is the biggest and the safest borrower in India which drives the demand side and also benchmarks the long-term interest rates, whereas RBI monitors the supply side of the money and looking at the inflation scenario in the country which further is dependent on many factors regulates the Supply of money through Monetary policies.

RBI controls the supply of money through Banking system by deciding on REPO rates and reverse repo rates. These are the rates at which RBI lends to Banks and let banks deposit their excess money with the banks. We will discuss more these rates later in future posts. But for now, just basic understanding of the supply of money is enough.

Now when you read in newspapers that RBI changes key interest rates, then that means that some action on Repo or reverse repo has happened which further will impact the deposit and lending rates of banks.

- Higher lending rates in banks refrain you from borrowing unless the business sentiments are positive.

- Lower lending rates mean RBI wants you to borrow more to increase the economic activity.

- Higher deposit rates means banks/RBI wants you to deposit your money to curb the money supply and thus curtail the inflation if that is proving hindrance to country at large

- Lower deposit rates mean banks/RBI wants to make banking deposits less lucrative for you and wants you to spend or invest more elsewhere to increase the economic activity.

This is what happens at the retail level, but when you lend to corporates or governments as in you buy their bonds, then they borrow for longer tenure to fund their projects and thus you require to keep money with them for long.

To provide liquidity to the investors generally longer duration bonds are listed in the stock markets so sellers may find the buyers and come out of their investments.

Now, longer the time frame, more will be the interest rate risk as you do not know which side interest rates will move and when. As we discussed above there are lot many factors which impact the interest rates movement.

(Read: All you wanted to know about Perpetual Bonds in India)

Due to this, longer the investments more volatile it will be. and that is why in the expectedly rising rate scenario it is advisable to invest in shorter duration bonds as you never know when you may get better rates than today and you want to lend or buy a bond at that price.

How do debt mutual funds operate?

I have tried to explain the workings of debt market in layman terms, hope I was successful in that and you have understood the crux of it if not the complete details.

Now when you invest in debt mutual funds the choice of fund is more important. Exposure to debt instruments is very important from Asset allocation point of view.

Debt mutual funds have products starting from Liquid funds with lesser than 91 days of maturity papers, to Long-term gilt funds with 8-10 years kind of papers.

Choice of funds depends on your objective and the average maturity of papers. If you need money after 1 year then there is no point being into a long-term gilt fund with 8 years of average maturity, as this might make your portfolio more volatile, the same way if your horizon is 10 years or more then being in short-term papers sometimes may not make sense.

This is the same manner as if you have longer investment time horizon and even the stock markets are looking volatile in near term then you should not just redeem your money completely and invest into bank FDs and keep waiting for the right time to enter. (Read: How to diversify portfolio through mutual funds?)

Now coming back to the question – Interest rates are expected to go up, which makes a point to invest in Short-term funds to see lower volatility and make money in the course.

But does that mean that we should shun long-term funds completely? and what about those who have already been investing or have invested in long-term debt mutual funds for a quite long time, should they consider switching the funds?

On the face of it, the answer is yes. But when you are investing in the Bond market through debt mutual funds where the fund manager also takes his calls on the portfolio looking at the interest rates scenario, then what? I believe the manager is better placed to understand the scenario well, at least in comparison to the retail investors.

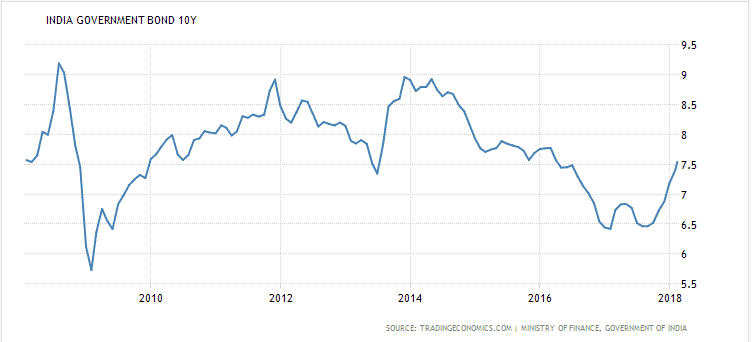

This leads me to look at the performance of Short-term debt, Long-term gilt and Dynamic funds for the past 10 years. In 10 years we have seen lots of interest rates volatility as depicted in the Graph below showing the 10years G sec rates for last 10 years.

Now Looking at the funds from 10 years perspective we might get a clear picture how your investments have got managed in the past, and what can we expect them in the future.

For this purpose, I have Randomly taken only those funds which have at least 10 years of track record. (All data is as on 12.02.2018)

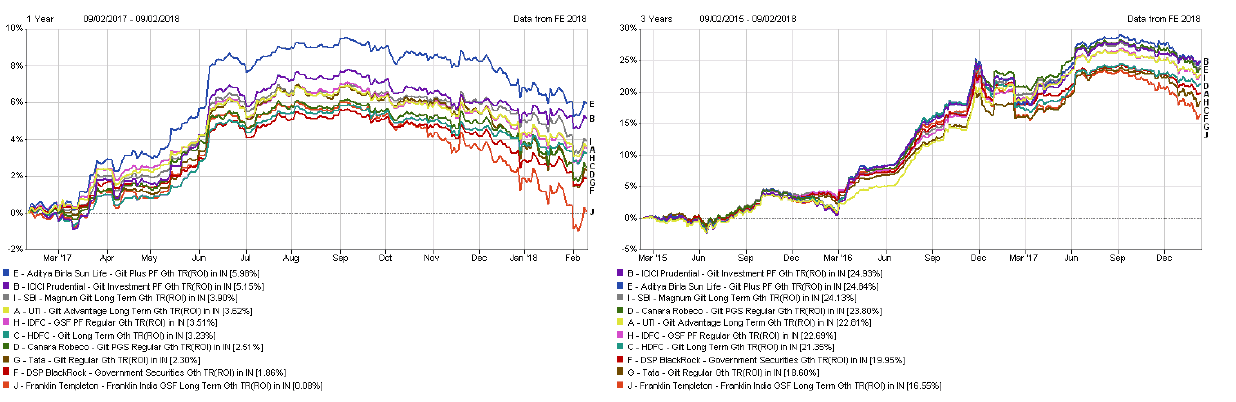

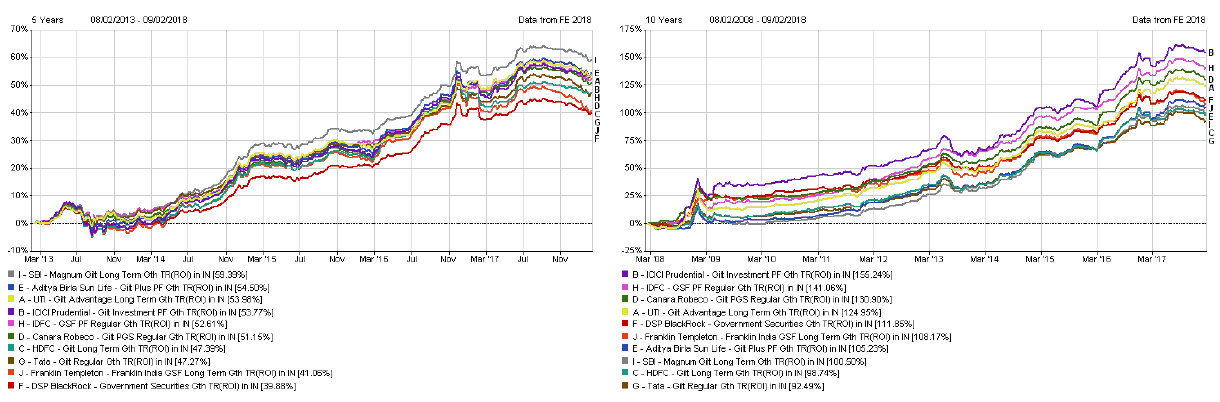

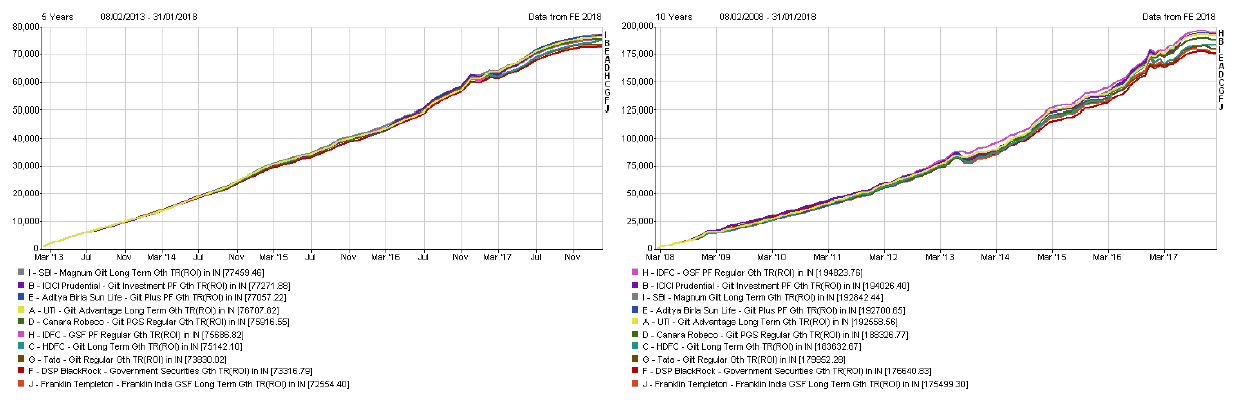

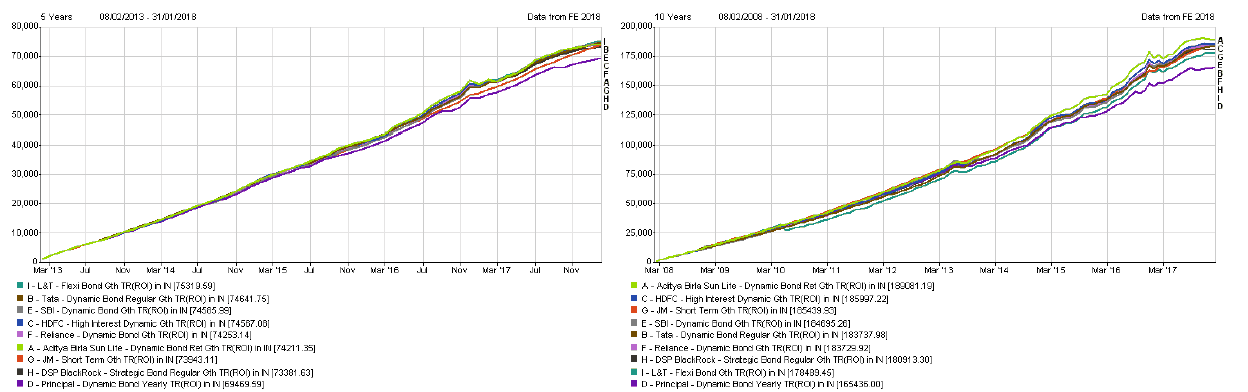

Debt Mutual funds – Gilt Funds

This is how Gilt funds have performed in last 10 (1,3,5 and 10 years) years, on lumpsum investment.

The above graphs show that where the best return any gilt fund gave in last 1 year was 5.98% (Aditya Birla), there the best performing fund in last 10 years has given 155.24% return or 9.82% CAGR. In 3 years and 5 years category, the best performing debt mutual funds have generated 7.70% and 9.77% respectively.

All this is when Gilt rates have remained quite volatile in past. One may argue that past 5 years we have seen falling long-term gilt rates, to which my answer would be in 10 years’ time frame we have seen rates going both ways.

You may also see the variation of rates in different years between different funds, like the lowest performing fund in all these durations has generated .08%, 5.23%, 6.94% and 6.77% in 1,3,5 and 10 years duration respectively.

Now here comes the role of monitoring the funds, so the corrective action can be taken as and when necessary.

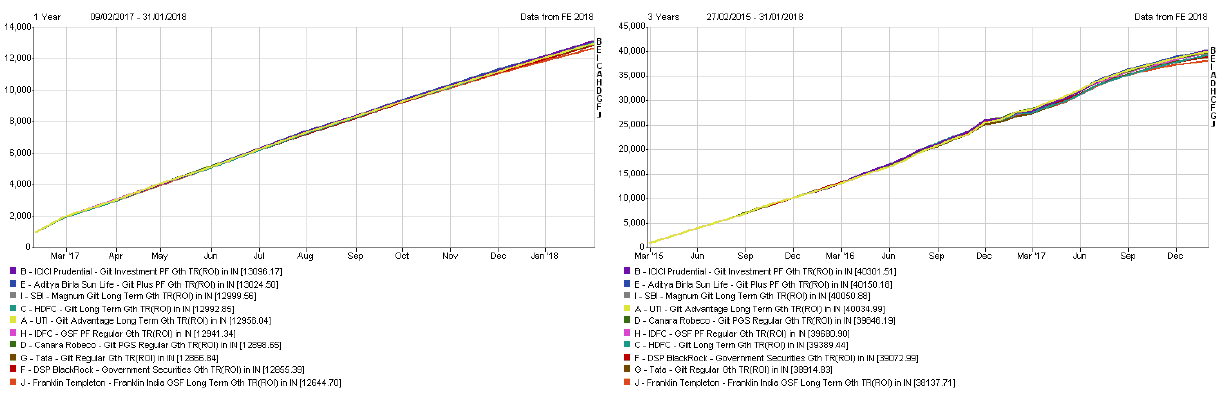

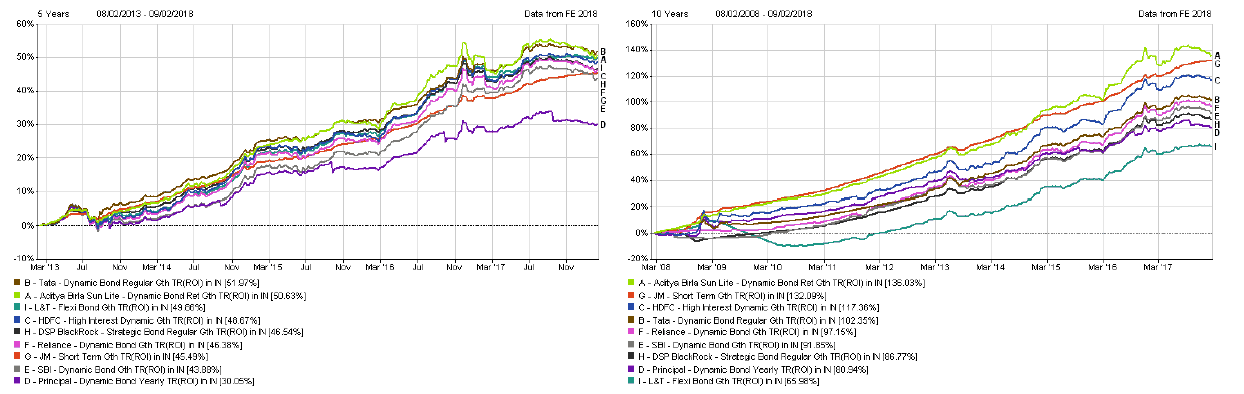

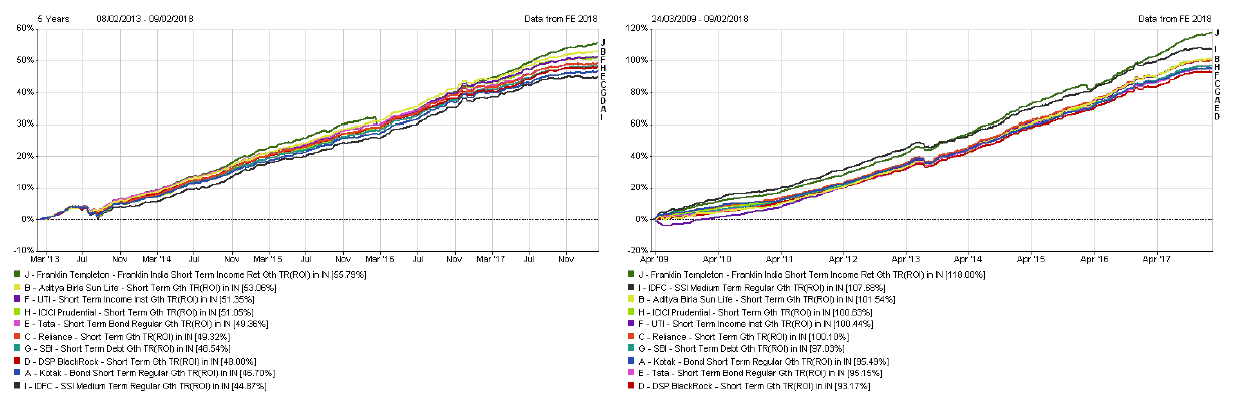

SIP in Gilt Funds

When the future looks uncertain and volatile than we always prefer to get into Equity through SIP (Systematic Investment Planning). How about Trying SIPs in Debt category of funds?

In the Same Gilt funds as selected above, below are the SIP returns chart with an initial and monthly investment of Rs 1000.

As per the charts above the best funds have delivered an annual return of 1.27%; 5.34%; 8.95% and 8.77% respectively for different time frames.

Let’s look at the same returns chart for Dynamic and Short-term funds to see, where they fit into the picture.

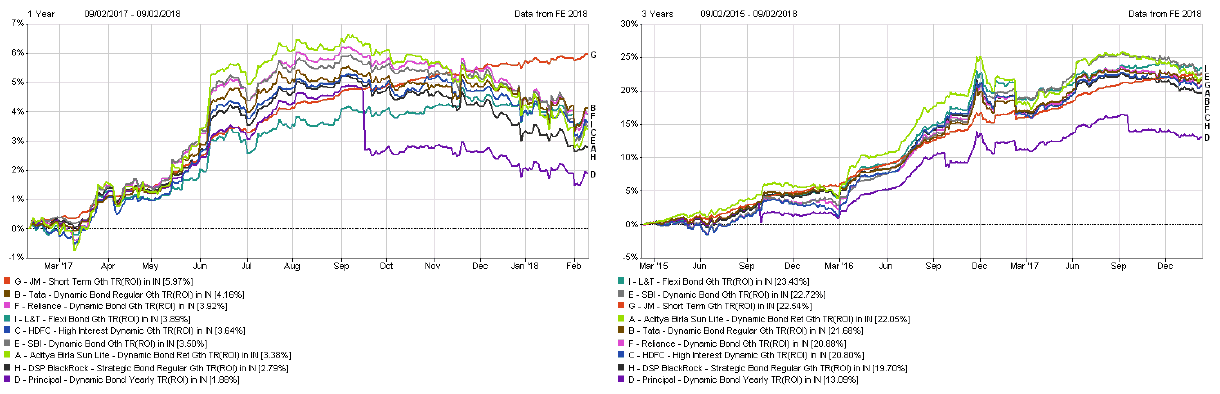

Debt Mutual funds – Dynamic debt funds

10 years Lumpsum investment and return chart

Dynamic funds are expected to take positions depending on the fund managers’ short to medium term view on the Interest rate scenario. In the last 3 years, they were having good exposure to the government long-term papers and was running on high maturity.

You can very well see, that for 1and 3 years’ time frame the returns charts of Gilt and dynamic funds looks quite similar.

10 years _SIP Charts

In case of SIPs, in dynamic funds, best returns range from 4.53% in 1 years’ time frame to 8.25% in 10 years’. For 3 and 5 years, the best returns have been 4.41% and 7.93% respectively.

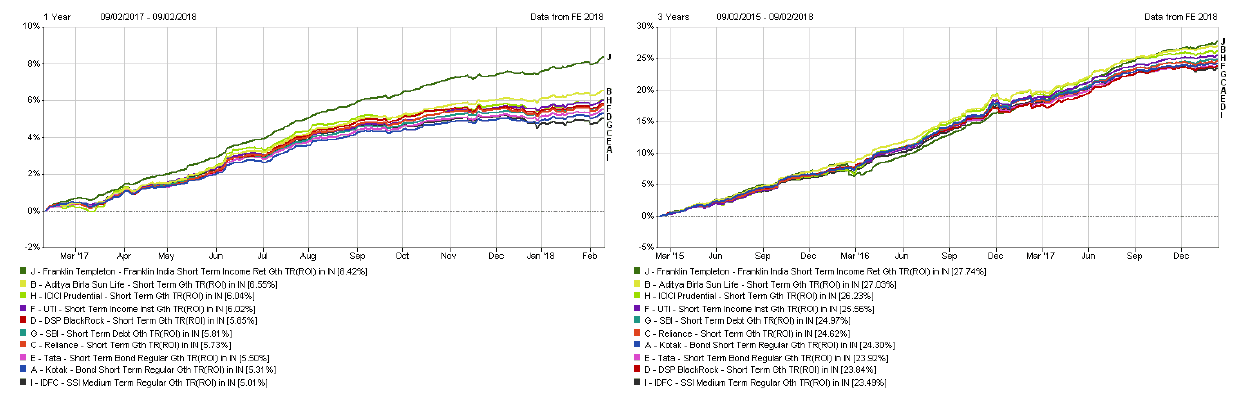

Now let’s look at Short-term funds, which are being advised today by many due to volatile scenario coming up.

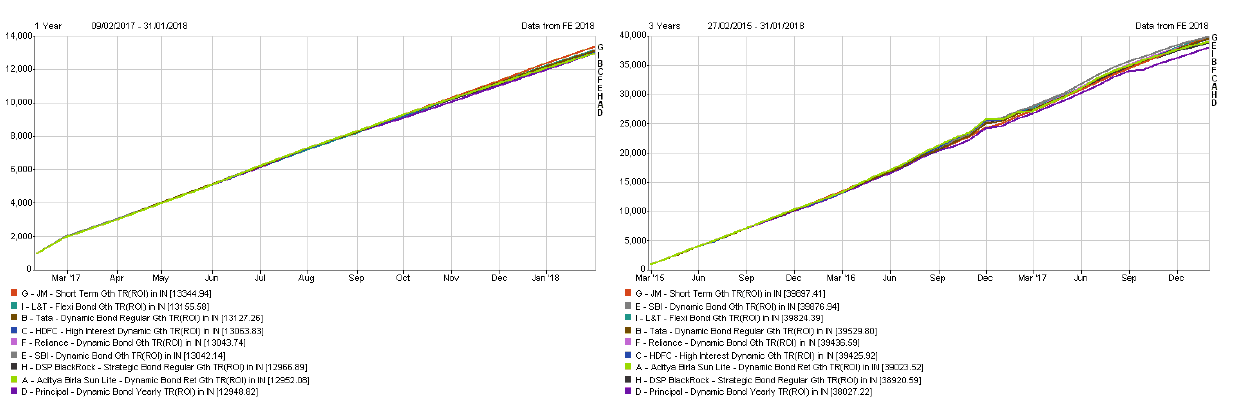

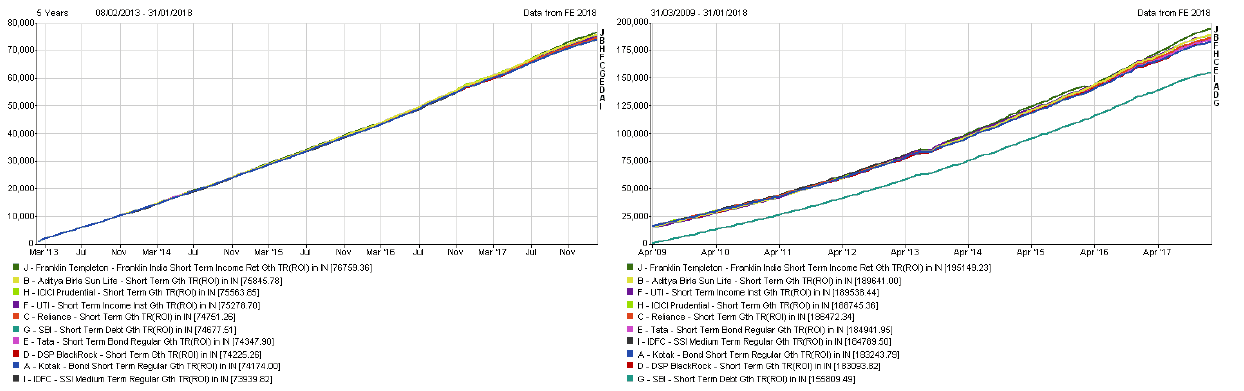

Debt Mutual funds – Short term funds

10 years lump sum investment and return chart

These charts clearly show that Short-term funds have clearly been laggards in long time frames. Check out the 10 years returns of Short-term funds with other 2 categories.

Moreover, the best fund that is coming up on the list of short-term i.e. Franklin India Short term fund is a Credit Opportunities fund though under a short-term category.

But the opposite is also true. Short to medium term return is equal or better in short-term funds in comparison to the other 2 categories.

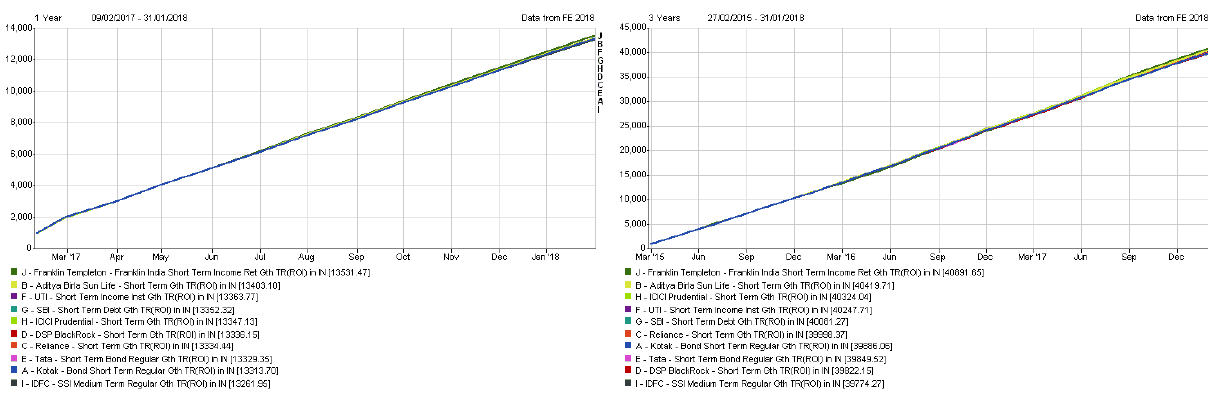

10 years SIP Chart – Short term funds

SIP in short-term funds has remained comparable to SIPs in the other 2 categories as mentioned above over a longer time frame. The best returns in different time frames have been 5.28%; 5.94%; 8.18% and 8.30% for 1,3,5 and 10 years’ time frame

Conclusion:

Past 10 years’ track record is enough evidence on how different categories of debt mutual funds have performed in different interest rate scenario.

Just like we cannot predict the future of equity markets as there are many factors impacting its returns, same way it is difficult to predict the interest rate movements over a longer period of time.

But unlike Equity in debt, we have very short-term to short-term instruments which can be used for near to medium-term goals.

But still, if you have very long-term goals and if past performance is to be believed, then there is no harm in going with Long-term funds too. If you have already invested, then I do not find any reason to panic.

Let the fund managers manage as per their View on Interest rates. However, it is important to keep monitoring the fund to timely weed out the not-so-good one from the List.

SIP for long-term in debt mutual funds may be a better choice to manage the volatility. But it is important to understand the taxation aspects too.

So, in the end, it is important to have a strategy at the place when you are dealing with investments. Strategy comes from your goals (Requirement), and risk profile. Follow a financial planning approach to be in the right kind of investments suitable to your goals.

If you have any questions on debt mutual funds, you may ask in the comments section below.

Manikaran Singal is the founder and Chief financial planner at Good Moneying Financial Solutions. He is a CERTIFIED FINANCIAL PLANNER CM and SEBI registered Investment adviser (Regd no. INA 100001620). He’s having 20+ years of experience in financial services space.

Manikaran Singal is the founder and Chief financial planner at Good Moneying Financial Solutions. He is a CERTIFIED FINANCIAL PLANNER CM and SEBI registered Investment adviser (Regd no. INA 100001620). He’s having 20+ years of experience in financial services space.")

{kind=link}

Dear Sir,

Have understood the categorization, but, not able to draw any ‘usable’ conclusion.

In view of expected rising/tightening interest rate regime, what I would like to understand is : I should invest in which fund. Means which type and which specific scheme/fund would give me maximum return in the next 3 to 5 years time frame as long as there is tight monetary policy in India as well as around the globe.

It further means, that, all long duration debt funds, which would have risen because of falling yield so far, their NAV would now, start falling and converse also. It also further means that if I have to invest now, I should invest in short/ultra short/liquid funds so that I can take the advantage of rising yield.

What I would like from you is your advice for investment in debt fund under various categories :

(A) For liquid/ultra short term : which fund/scheme.

(B) For income fund : which fund/scheme.

(C) For long duration income/debt fund : which fund/scheme.

regards