Understanding calculations behind Income from house property is imperative for those who are catering to a home loan on their self-occupied or investment property, and even for those who are planning to buy new property by taking a home loan.

Buying house property has always been looked at as one of the tax-saving tools citing a reason to claim home loan tax benefits. But budget 2017 announcements limit the benefits of buying the second property. In fact, it is going to affect more to those who are already paying EMIs on their let-out property and have been claiming Interest payment benefits under section 24.

This article will give you a basic understanding of how to calculate income from house property with specific reference to the new rules announced in budget 2017.

Before going further, let’s first understand what house property means as per Income tax rules.

Income from House property – What is House property

House property is a building and land attached to it if any. A Building can be in any form like a Residential house, flats, shops, farmhouse, factory sheds, and land attached also can be in the form of a playground, compound, car parking, garden etc.

It does not constitute an open plot of land whose income may be charged under Income from other sources or Business Income.

For a property to be taxed under Income from house property, it needs to satisfy the following 3 conditions:

- It must consist of Building and land attached (if any)

- The assessee must be the owner of that property.

- The said property must not be used for own Business or profession, the profits of which are chargeable to tax.

Income from House property – Self Occupied and Let out house

In Simple terms, if you use the said property for own residence then that is called as Self Occupied property. If you have put that property on Rent to some other person then that is let out property.

If you have more than 1 property and even if the second property is not put on rent, still as per Income tax rules, one of your property will be considered as Self Occupied and other is “deemed to be let out”. But it is your discretion which of the property you want to show as self-occupied or let out.

Deciding between self-occupied and let out property, used to be a very important decision because of the limits defined under home loan tax benefits to claim interest on housing loan deduction under section 24.

As per section 24(b) of income tax act, in case of self-occupied house you could deduct upto Rs 2 lakh of home loan interest to calculate the Income from house property, whereas in case of let out property there is no limit on Home loan interest deduction and assessee can claim entire interest on housing loan to calculate tax on rental income in a financial year. (W.e.f 01.04.2017 the limit on Home loan interest deduction has been revised)

This was the main attraction behind buying second house property, as by claiming entire interest outgo out of your taxable rental income, on one side your overall income tax liability reduces considerably and on the other, you have made an investment in a growing Investment asset class at a lower effective cost.

But in Budget 2017, Government has restricted setting off “Income/Loss from House property” to Rs 2 lakh only. We’ll discuss this in the later part of this article.

How to calculate Income from house property

Here you need to first understand few terms before moving ahead with actual calculations.

Annual Value

The first thing is to find out what exactly are you actually earning from that property. This is called as Gross Annual value. Gross Annual value is the capacity of the property to earn Income.

If you are actually receiving rental income from that property, then that will be called as Annual Rental value. But there are 2 more annual values that need to be considered, which are:

- Municipal Annual value – This is the value assigned by Municipal authorities, based on which they collect Municipal taxes.

- Fair Rental value – This is the rent which similar kind of property, in a similar area would fetch.

Higher of Actual Rent received/Receivable, Municipal annual value or fair rental value will be considered as Gross Annual value for making final calculations towards Income from House property.

Whereas if the Rent control act applies in your area, then the Annual Value would be Higher of Standard Rent (as fixed under the act) and Rent received.

Besides Annual value, there are some other important things to learn about calculating Income from House property.

Municipal taxes – These are to be deducted from your Annual value, to reach Net Annual value of your property.

Standard deduction – This is the deduction which is allowed for repairs, rent collection etc. irrespective of actual expenses incurred. The deduction is 30% of Net Annual Value. No standard deduction is allowed in case of NIL Annual value as in the case of self-occupied property.

Interest on Housing Loan – The interest portion of home loan EMI is allowed to be deducted from the Net annual value.

In the case of self-occupied property, the Limit is Rs 2 lakh u/s 24 Plus Rs 50000 if section 80EE applies. ( Read: all about Home loan tax benefits)

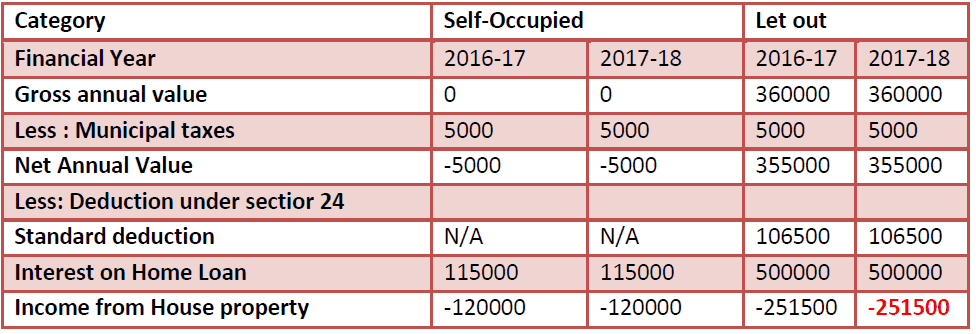

In the case of let out property there used to be no limit on interest deduction and assessed can claim complete Interest outgo in a financial year. But, w.e.f. FY 2017-18 though assessed can deduct the complete interest from net annual value, not more than 2 lakh can be set off with other income heads to calculate the gross total Income and balance loss can be carried forward to next 8 years to be set off against future Income from house property only.

Let’s understand the complete calculation through an example

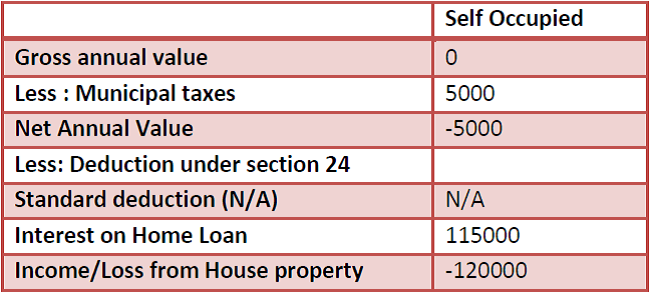

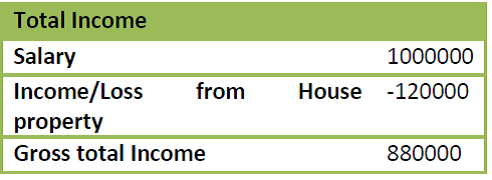

Case 1 – X has a taxable Salary income of Rs 10lakh per annum. He is living in self-occupied house property and paying Home loan EMI of Rs 35000 per month. His total Interest outgo in a financial year comes out to be Rs 115000. What would be the taxable Income from house property and total taxable income?

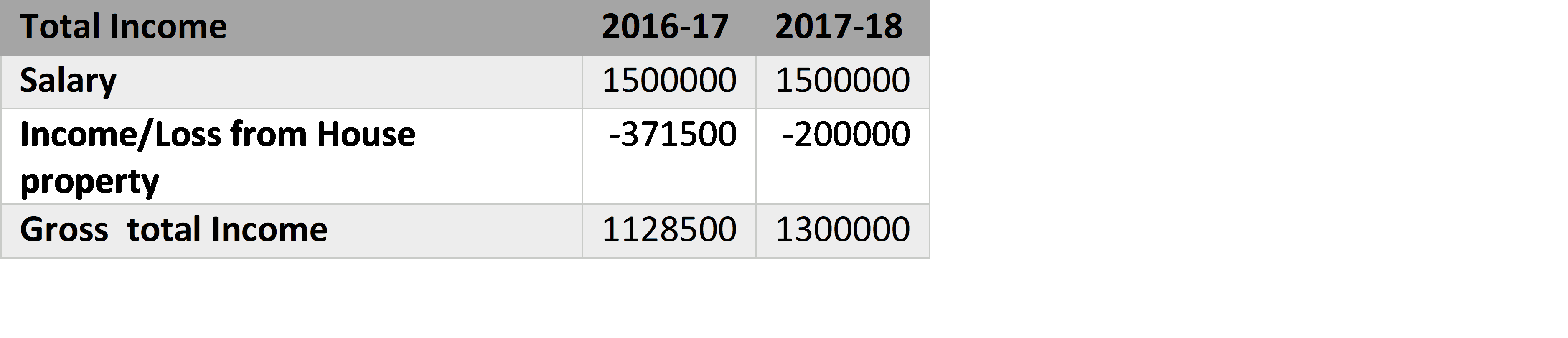

Case 2 – X has taxable Salary Income of Rs 15 lakh. In addition to the property above, X also bought another house property on loan. He is getting Rent of Rs 30000 per month which is a fair rent in the area. He is paying EMI of Rs 60000 per month. His total Interest out go on housing loan of the second property was Rs 500000 in a financial year. Calculate his taxable property income as per old and new rules

Conclusion

You can very well see from the above calculations that in new rules effective from 2017-18, it would not be wise to buy a second property with the heavy loan amount because the benefits are limited now.

But one thing you have to keep in mind is that it is you who have to decide which property to keep as self-occupied and which let out and you can change this decision every year, looking at your tax profile. So with a bit of tax planning, you may work out your Income from house property in favor of you to maximize the tax benefit.

Other ways to increase the tax benefit can be taking a Joint loan, buying property in joint ownership. Since your empty houses will also be taxed as deemed to let out so, it’s always better to keep your properties let out always and keep earning rental income.

Income from house property is a vast topic, with so many intricacies. I have covered only the basics of it. Would love to have your questions and discuss more on this subject.

Manikaran Singal is the founder and Chief financial planner at Good Moneying Financial Solutions. He is a CERTIFIED FINANCIAL PLANNER CM and SEBI registered Investment adviser (Regd no. INA 100001620). He’s having 20+ years of experience in financial services space.

Manikaran Singal is the founder and Chief financial planner at Good Moneying Financial Solutions. He is a CERTIFIED FINANCIAL PLANNER CM and SEBI registered Investment adviser (Regd no. INA 100001620). He’s having 20+ years of experience in financial services space.")

{kind=link}

I have another variation to House Property Income Tax calculation.

It pertains to one of my relatives, who has 2 houses in a Metro City,without any housing loan liability(loans fully PREPAID).

He works in another Metro and resides in a Rented Property.

How to compute the Tax,especially with regard ton Self occupation.

What i understood is that he has 2 properties in a metro city, but lives in another metro on rented accommodation, Right?

He can keep one of the properties as self-occupied and other would be let out.

If there’s no loan going on relating to the self-occupied property then there would not be any gain or loss, so there’s no tax liability and Income would be NIL in case of the self-occupied house.

I have two houses. Previously I was paying on deemed rent basis. I want to know should I pay or not on second house where partial year rent received due to tenant vacated house in ft 2019-20. Thanks.

having one flat at hyderabad and given for rent. and i am staying at chennai by paying rent to other