If you have any life insurance policy, then recently you must have received a mail from your insurer regarding the TDS on life insurance policies to be deducted out of your policy proceeds. I have been receiving many queries regarding this, saying they are feeling cheated since at the time of buying they were told that the policy proceeds will be tax-free.

Though I have answered them as per the respective policies they have, it is important for all of you to know about the change in taxation law which was announced in the Budget 2014. To remove the confusion I have written this detailed post on TDS on life insurance policies.

Tax laws related to insurance policies

Life insurance policies are structured around 2 income tax sections. Section 80C and Section 10(10)d.

If the Life insurance policy you have, be it ULIP or Endowment, is providing you insurance cover of 10 times of your annual premium, then you can claim tax benefits under both the above-mentioned sections.

You can claim a tax deduction on the premium paid in last financial year u/s 80C up to a maximum limit of Rs 1.50 lakh, and also the maturity proceeds you get will be tax-free u/s 10 (10d). (Read: All qualifying Investment and expenses under section 80c)

In other words, if the premium you are paying is 10% or less of the sum assured/death benefit then you can enjoy the benefit of section 80c and 10(10d).

Important: If the policies were bought before April 2012, then to claim benefit under 80C and 10(10d), your insurance cover should be at least 5 times of annual premium.

But if your policy is not satisfying these conditions then your 80c benefit would be restricted to 10%/20% of sum assured as the case may be and your policy maturity proceeds will not be tax-free under section 10(10d)

Let’s understand this in some cases:

Case 1: Rajan has one Life insurance policy, bought in 2005, with an annual premium of Rs 50,000/-. The policy has sum assured of Rs 3 lakh. The policy is due to mature next year in 2015. He wants to know if the maturity proceeds are taxable?

Answer: NO. As the policy was bought before April 2012 and has sum assured more than 5 times of premium amount, then it satisfies the condition of section 80C and 10(10d) and thus is not taxable.

Case 2: Samar has bought one pension plan in 2007, with an annual premium of Rs 10,000/-. It doesn’t have any sum assured attached to it. What would be the taxability of this policy on maturity?

Answer: As theirs is no sum assured attached to this policy then it doesn’t attract section 10(10D) and thus the maturity/surrender proceeds will be taxable. However being a pension plan, the premium payments come under section 80CCC, and he can enjoy the tax benefits on premium payments.

Case 3: Last year in 2013 Simran bought 2 policies, one a pension plan for her retirement planning and other one ULIP for investments. In a pension plan, she’s paying a premium of Rs 20000 and has insurance coverage as “higher of fund value on the date of intimation of death or 105% of premiums paid”. While in case of ULIP she is paying a premium of Rs 1,00,000/- and having a cover of 15,00,000/-. She want to know the taxability of these policies on maturity?

Answer: Though Simran has some insurance cover in case of pension plans this is not satisfying the condition of 10 times of annual premium. The other ULIP policy has sufficient cover.

So in case of the pension plan maturity proceeds or even the monthly pension amount is taxable, but in case of ULIP maturity proceeds will not be taxable.

Case 4: 2 years back in Jan 2012 Rahul bought one single premium plan, with an insurance cover of 1.25 times of premium, he wants to withdraw the policy after completion of 3 years. He wants to know if the Maturity proceeds would be taxable.

Answer: Yes, the maturity proceeds would be taxable. Since the policy was brought in Jan 2012, so in this case the policy should provide a cover of at least 5 times of annual premium, to make it tax-free.

Applicability of TDS on life insurance policies

TDS on life insurance is applicable on the maturity proceeds of taxable policies, as explained above i.e which are not satisfying the condition of death benefit/Sum assured equal to or more than 10 times of annual premium.

Finance Act 2014 has introduced a new TDS provision under section 194DA in the Income Tax Act, 1961 on insurance policies

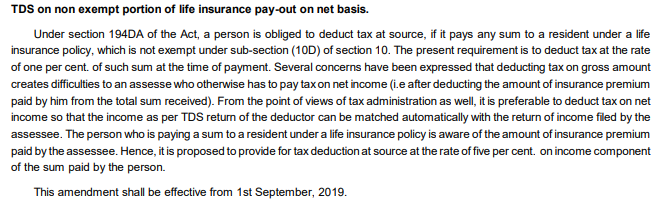

As per the new section (effective from 1st October 2014), if the policy proceeds are not eligible for exemption under Section 10(10D) of the Act and your total payout value (policy proceeds due ) w.e.f 01.09.2019 the TDS will be deducted only on the taxable value of Policy i.e. less the premium paid (check the excerpts as per Budget 2019 memorandum below) , for the proceeds exceeding Rs. 1 lakh.

TDS will be deducted at the rate

- At 5% (for valid Pan registered)

- At 20% (for valid PAN not registered)

- In case of NRIs, TDS gets deducted at maximum marginal tax

Earlier the onus is on the policyholder to disclose the type of policy and pay tax(if any) on the maturity proceeds, but slowly this has become a point of tax evasion. Many people evade it knowingly and others under ignorance. This TDS on life insurance policies would automatically plug this issue and bring the attention of taxpayers and income tax authorities on the taxability of maturity proceeds

(Also Read: Tax Implications when you discontinue Life insurance policy)

TDS on Life insurance policies – What to do?

TDS on life insurance policies is applicable from 1st October 2014. There’s nothing much policyholders can do now about it, but those who now know that their policy is taxable should get their PAN number registered with the insurer to avoid getting 20% TDS deducted.

Disclaimer: I am not an Income tax expert. The Information shared in the article and the comments below are to the best of my understanding, from different sources, articles, and discussion with other experts on this subject. Before acting on any of the statement, do consult a tax professional.

Manikaran Singal is the founder and Chief financial planner at Good Moneying Financial Solutions. He is a CERTIFIED FINANCIAL PLANNER CM and SEBI registered Investment adviser (Regd no. INA 100001620). He’s having 20+ years of experience in financial services space.

Manikaran Singal is the founder and Chief financial planner at Good Moneying Financial Solutions. He is a CERTIFIED FINANCIAL PLANNER CM and SEBI registered Investment adviser (Regd no. INA 100001620). He’s having 20+ years of experience in financial services space.")

D which makes){kind=link}

Informative post. But what happens to ULIPs which are eligible for tax exemption u/a 10 (10 ) D , but is withdrawn before maturity or completing the term i.e surrendered prematurely once the lock-in period is over? Will TDS be applicable ?

Thanks Annapurna. The answer to your question is NO.

If the product is eligible for tax benefit u/s 10(10)d, then no TDS will be deducted even at the time of premature withdrawal.

query pertaining to ICICI Pru Lifetime Super Pension & Premier Life Pension , Policy held with ICICI Prudential Life Insurance Company Limited.

The policy was issued on February 2, 2008 and 23, 2009 along with the first premium deposit for the said policies.

I want to surrender the policy. As per the product norms surrender Value is payable after the policy has completed 3 years and the premium have been paid for 3 yrs.

One policy is full NRI funds, second policy 1/4 is NRO funds. ICICI pru

First policy deducted TDS 30%

Premium paid 30lac in 2008 and 2011 for first policy deducted TDS and are paying amt Rs36,12,750.

Letter stated zero TDS

Premium paid for 5lac second policy 2009 and 2013 for second policy a sum was paid by DEmand draft for which we are able to find the sorce but are ready to to say it’s NRO just bcz the banks are not cooperating in giving information.

Amt yet to pay Rs 894146.

I live abroad since 1998/9 till date.

Since a month am trying to get the surrender Amt. but either ICICI has not submitted repatriation letter or are unsuccessful in NEFTS which was my first request.

TDS has been debuted but letter issued states 0.00 is this ethically right,

Every day I spend time on phone or email but in vain. Hardly get responses. Their greivece dept is as good as dead.

Is Icic right in deducting tax for NRI funds if yes are they right to state zero.

Thanks for reading and if you are able to respond.

Regards

Well i can understand how difficult it would be for you to deal such matters sitting abroad. Frankly since i am unable to understand your complete query, what i can reply on as per my understanding is that Insurance companies are right in deducting TDS on taxable Insurance policies ( especially in case of NRIs, but then they cannot write TDS decuted as ZERO. They need to provide you with complete details as to what has been deducted and for what.

If you are not happy with the solutions provided by the grievance department, then you may approach Insurance Ombudsman http://www.policyholder.gov.in/Integrated_Grievance_Management.aspx

There are two aspects to the issue:

1. tax deduction under section 195 applicable to Non residents; and

2. The amount, which becomes taxable i.e. the whole amount received including the principal, or the surplus u/s 10(10D).

For point 1, my opinion is that ICICI is correct in deducting tax ‘at the rates force’ which are slab rates applicable. In absence of other details they have deducted tax@30% ( section 194DA is applicable to residents only)

Point No. 2 – In my opinion, only the gain should be taxable. Any tax advantage u/s 80C should be added back. Now the next part of it is, if the surplus or gain is taxable as long term gain since the investment was held for more than three years, and if yes; can benefit of indexation be taken?

In my opinion again, I would say ‘yes’ to both the questions.

I have tried to find answers to above questions from various insurance companies but no one is ready to provide clear answers and toss the ball back to me being a tax advisor!

My painful disclaimer is that, these are my opinions and hence personal judgment needs to be exercised before acting on them.

Hello Sir,

I have a question regarding my ICICI Pru life Super pension.

I started this policy since 2016 with an annual premium of 10,000 and assured maturity value of 1,00,000. And some years instead of 10,000 I contributed more for tax benefits.

Currently it is showing the total contribution is 1,80,000 and the maturity value is 2,57,372. Since it is matured this year I wanted to withdraw the matured amount, but the Insurance office staff is telling it will attract TDS at 20% because it is a Pension plan. And inorder to avoid that they were suggesting me to either continue the policy or a portion of the amount to reinvest in one of their policy.

Since I have no plans to further investment at this moment, suggest me what should I do to avoid tax deduction.

Thanks,

Manoj

I think you have quoted wrong start Year…you seem to meant 2006.

See, pension plan is always taxable. It is not subjected to 10(10D) condition. But still, i have seen in many cases, insurer don’t deduct any TDS on pension plans, unless the insured is NRI. But even if they don’t deduct any TDS your policy would remain taxable.

20% TDS is applicable only where your PAN is not updated with the insurer. I would recommend you to update your PAN in their records.

And don’t fall into the trap of buying new policy, as even this would not save you from paying taxes on your pension plan.

Hello Sir,

You are right! Sorry it is 2006.

Thanks for your suggestion! But let me know is there any way I can avoid deduction of TDS. They suggested me that if you are continuing this policy then no need to pay TDS.

Thanks for all your support.

Best,

Manoj

Yes they are right. TDS or Tax in any form gets applied only when you book some profit or earn some income. Notional income does not get taxed. But do remember, whenever you get the proceeds it will be taxable. So if you need money now, there’s no point keeping it pending for future. But if you don’t need money now, then you may wait for its maturity, then you may ask for 1/3rd of the proceeds as commuted pension ( tax free) and rest with 2/3rd of the balance you need to buy annuity and start getting pension.

Do read out the policy document for this clarification.

Dear Manikaran,

In case an insurance policy does not fulfill the conditions of 5 times or 10 times, the benefits of section 80C are available but restricted to as much as 10%/20% of capital SA and not denied altogether. For example if SA is 1 lac and premium is 10200 ( DOC=post 01.04.2012) then 10000 (1/10th of 1 lac) is eligible. Kindly refer to your article above “But if your policy is not satisfying these conditions then neither you will get section 80c benefit, nor policy maturity proceeds will be tax free under section 10(10d)”

Oops!! Yes Mr. Gupta. You are right. Thanks for pointing this out.

I invested in ‘LIC Wealth Plus’ in the year 2010 with yearly premium of Rs. 50000/- where section 10(10D) is applicable. Now I want to surrender the policy and withdraw the money. As per the new tax section will TDS be deducted from the surrender value?

If your insurance cover is 5 times of your premium then no TDS will be deducted on your policy surrender value. You may also check this from LIC operation guys before punching in your request.

Dear Sir,

I am Gnanakumar from Coimbatore.

In June 2011, I got a smart insurance plan 3 policy in Bajaj Allianze. The yearly premium is 100000 and sum assured is 1000000. The premium payment is for 6 years and maturity in 10 th year.

I paid 5 premium and I planed to surrender it now.

They are telling that 2% TDS is applicable for the value.

Is TDS applicable for this policy.

Please help me

Thank you.

If the policy is inforce and you surrender after completion of 5 years, i think there should not be any TDS deduction. There may be some surrender charges but not TDS. Your Sum assured to Premium ratio is within the limits of section 10(10)d, so the proceeds should not be taxable.

I have taken a policy with ICICI prudential called elite pension for 5 lakhs one time payment with sum assured is zero. This policy is taken in Dec 2009 and it is for 6 yrs and ends Dec 2015. After 5 yrs, i.e. Dec 2014 the surrender benefit is 100%. I was not sure that time about ULIP etc, I took this as investment and now reaching to 5 yrs and it is touched 5lakhs 10 thousand. I am not happy with this product and planning to withdraw after 5 yrs to get atleast my money back. Will TDS applicable on this payout and I have to pay any tax on this payout. If you can give your input it would be great. Thanks and appreciate for your reply.

Raghurama, Insurance policy with no sum assured will definitely attract TDS.

Even if the policy was taken in 2009, then also to make the maturity tax free under section 10(10)d there should have been a minimum sum assured of 5 times your premium.

Now whether your total amount is taxable or only Rs 10k…this has to be seen. My view is that as Rs 10k doesn’t come under capital gain and neither it comes under interest earning, so the whole amount i.e. Rs 5.10 lakh would be taxable.

You would gain more clarity on this taxation when you surrender the policy and TDS gets deducted. If TDS gets applied on Rs 10k then you have to add only Rs 10k in your income and pay tax s per slabs, otherwise add the total amount in your income.

My view is that it would be fully taxable under 80CCC and have to be added to his income and pay tax as per slabs.

Whether TDS done @ 2% on ULIP claims is eligible for indexing at the time of filing income tax returns so that we can claim back the TDS , provided the result of indexing is a loss ?

Sanjay, ULIP gains/Losses does not come under Capital gain/loss, so there’s no question of indexing.

Sir, please clarify if the ULIP policy is held for more than 3 years. In such case whether maturity amount will be treated as capital Gains or not?

Hi,

I bought a ULIP policy on 24th march 2007, the sum assured is 125000 and the annual premium is 23000. Since the annual premium is always less than 20% the maurity/surrender amount is tax free right. Please clarify.

I am planing to purchase 817 no table for 11 yr term by giving 77000 prem and availing 1 lac cover for father aged 63 does it qualify for tax exemption under 80c and 10(10)d

Without commenting on table number, the bottom line is that sum assured should atleast be 10 times of the annual premium. In your case it doesn’t seem so. So the maturity proceeds would be taxable.

Dear Sir, I am planning to buy a single premium pension policy about 1.0 crore under LIC Jeevan Akshay scheme. My current status is NRI but have plans to relocate to India in a one or two years time.

Appreciate, if you please let me know how tds would work on the pension amount on monthly basis which should be around INR.75000/-

Regards,

Rajesh

As per section 194d , 2% tds is applicable on policies where maturity, surrender or survival is taxable and the annual payout is more than Rs 1 lakh.If Pan number is not submitted to insurer then tds will be @ 20%. Pension plans in any way are taxable policies.

Thus i think Rs 75000/- per month will be subjected to tds of 2%. At Year end you have to club the total amount received in a year along with other taxable incomes and pay remaining tax as per the income tax laws at that time after adjusting 2% already deducted.

Many thanks sir for reply. Its very informative and helpful for planning.

Regards,

Rajesh

You are most welcome Rajesh. Keep coming and keep sharing.

As provisions of section 194DA are not applicable to pension plans like Jeevan Akshay, on annuity payouts under Jeevan Akshay are not subject to TDS but recipient of Annuity will pay taxes as per his applicable slab.

yes correct, for NRI s the section is 195 and deduction of TDS subject to DTAA

Dear Manikaran Singal,

Your information is very informative and helping people.

In year 2004, I purchased a ULIP policy of annual premium Rs. 20,000 and Sum Assured Rs. 200,000. I paid 6 premiums till year 2009 on time. In year 2010, I hadn’t paid premium and did partial withdrawal of Rs. 110,000. Currently, I am not paying premium since year 2010.

Recently (few days back), I surrendered the policy and found insurer had deducted 2% TDS from surrendered amount. After talking to insurer I got to know that in year 2010 they reduced sum assured by partial withdrawal amount. Insurer is not confident whether TDS needs to be deducted or not but they did on safer side. Now, I am confused whether I need to pay tax on surrendered policy amount because when I was paying premiums my sum assured was Rs 200,000.

Please help me to come out from this situation.

Thanks

Sunil

Dear Manikaran Singal,

Please look at me query and clarify.

Thanks

Sunil Aggarwal

Here’s my take. You buy the policy with 10 times of sum assured and whatever you have paid and till whenever you have paid the condition of 5 times of annual premium cover is getting maintained. So your policy is fulfilling all the requirements of coming into tax free status.

It is only in 2010 you made partial withdrawal. But this also should not make your policy taxable, as this is just the policy feature that you have used.

Reduction of Sum assured based on withdrawal depends on policy conditions which you have to go through once, but unless specifically mentioned partial withdrawal doesn’t make your tax free policy taxable.

Still i would advise you to consult a good tax lawyer / Chartered Accountant.

Thanks a lot Mr. Manikaran Singal.

I appreciate your response.

Regards

Sunil

My question is that if the policy holder is having NRI STATUS and premium were debited from his NRE A/c. then NRI is liable for tax under the new IT rule effective from 01/10/2014 or not ? If NRI is liable then what will be the Tax percentage ? Tax will be deducted on total payout or only on gain portion ? Please clarify.

-If the policy is taxable as per rules, then it would definitely be applicable to TDS. It doesn’t matter if the policyholder is NRI or Resident Indian.

-Same percentage as in case of resident individual – 2% if PAN is there else 20%.

-TDS will be deducted on the total payout value if exceeds Rs 1 lakh in a financial year.

There’s one recent provision announced in the latest budget 2015, that if a policy holder finds that there ‘s no other sources of income for him and thus his taxable income ( including the policy proceeds) is going to be below the basic exemption limit then he can submit form 15g/h to the insurance company and avoid getting TDS deducted. But i am not sure if this benefit is available to NRIs or not

Dear sir,

I am a NRI I have taken a single premium policy during March 2010 paying the premium of Rs10 lakhs with insurance cover of 1.1 times (Rs 11 lakhs) the premium was paid from from my NRE account. Now after completion of 5 years I wanted to surrender this policy. The insurance comapny is saying that there will be a TDS on my policy @ 30.9% for the profit amount( fund value – premium paid) Is this TDS applicable for NRIs please give a clarification.

Antony, though i was under impression that the rates of TDS in case of LI policies for resident Indian and NON resident Indians are same. But after your query i did some research on this subject an found that in case of NRIs TDS rates applicable on taxable insurance policies is 30% as per section 195 of IT act. Check the link below.

http://www.idbifederal.com/TaxBenefits/Pages/TDS-U-s-194DA-on-Life-Insurance-Proceeds.aspx

One thing i am still not clear, as what insurance people told you to deduct TDS on profit amount, but in my view it should be on full surrender proceeds as the complete amount is taxable in this case and not only the profit.

Once you are through with this transaction, do share exact happening.

Hi ,

I paid 30.9% on the Total amount – premium . its a pension policy and there is a clause .

The premiums paid by you for this plan

are eligible for tax benefits under Section

80 CCC as per prevailing tax laws.

IS THIS CORRECT TDS RATE NOW:

TDS Rates for Non-Residents u/s 195 of Income Tax Act, 1961

Sr. No. Nature of Payment Co. Others

1. Long Term Capital Gains u/s 115E NA 10%

2. Other Long Term Capital Gains (excluding u/s 10(33), 10(36) & 10 (38)) 20% 20%

3. Short Term Capital Gains u/s. 111A 15% 15%

4. Investment income from Foreign Exchange Assets NA 20%

5. Interest payable on moneys borrowed or debt incurred in Foreign Currency 20% 20%

6. Royalty & Fees for technical services u/s. 115A

– Agreement 1st June, 1997 to 31st May, 2005

– Agreement on or after 1st June 2005 20%

10% 20%

10%

7. Winnings from Lotteries, Crossword Puzzles and Horse Races 30% 30%

8. Any Other Income 40% 30%

Pension policies are eligible to claim tax benefits u/s 80CCC which is applicable on Investment amount, but the withdrawal is always taxable. and as these days TDS is applicable on taxable insurance products so the proceeds will be adjusted to tax applicable. In case of NRIs. TDS would be at maximum marginal rate i.e. 30.9%

as per circular TDS is applicable for NRI s as per DTAA of that country

Dear Sir

Really impressed with the way you are replying to your readers query. Hats off to you for your patience and interest. My query is in case of NRI is 30% TDS deductable even after submitting PANCARD?

Yes Andrew. NRIs are subjected to deduction at maximum marginal rate.

If the policy is not 10 10 D complaint, secondly TDS will not be deducted if NRI is tax resident of any of the countries covered under DTAA subject to funishing of form 10 F and tax residency certificate.

Sir,

Case- Policy bought on 01.02.2013

1. endowment plan term: 5 years, Monthly premium- 10810, Sum assured- 600000

bonus is around 20400 per year

What would be tax liability scenario in this case as yearly premium >10% of SA. And what about the maturity proceeds that would be around 700000. Would this whole proceed be tax liable

Leave aside bonus Amit, at annual premium of Rs 129720 ( Rs 10810 monthly), your sum assured should have been 1297200 to make the maturity proceeds tax free. Now whatever you receive on maturity will be taxable and subject to TDS

Dear sir

I have taken LIC policy in oct2011 under money back scheme with yearly premium of 29500/- for insurance cover of 800000/-. As per policy, 10% of amount will be paid to me on completion of every four year. So I will receive 80000/- on this oct 2015. I want to know whether this amount is taxable or TDS will be deducted by LIC. Thanks

No, money back amount will not be subject to TDS. Moreover your policy is well within the tax free limits as 29500 premium with 8 lakh sum assured, so i don’t think there’s need to worry.

Hi, If my Insurance policy was issued in 2009 with Annual premium of Rs 20000 and SA of Rs 100000, and at the time of surrendering the mode is monthly with amount Rs 1667, would TDS be deducted? (As per me it should not be, however as per insurer, it will be since 1667 X 12 = 20004)

Even I think so Anurag. It should not affect the taxability.

Hi, Got back my TDS deducted amount back from my insurer. They calculated TDS on premium paid instead of Annualized premium.

Thanks for your response

I have jeevan shree which was bought on 28-1- 2001 sum assured 500000 and premium is 25000 then is there any tds will be deducted on maturity amount @ on 28-1-2024

No Nitesh. 5 lakh of sum assured equals 20 times of 25k, which is very much with in limit prescribed. So there should not be any TDS.

I am having a 10 year pension policy with [email protected] since 2008.I have not taken any income tax benefit on the premium paid.In case I surrender the policy now I am likely to get an amount of Rs.3.25 Lakh.Since I am in the tax bracket of 30 %.So if I have to pay tax on the surrender value I have to pay tax of about 0.975 lakh and I get only Rs.2.275 Lakh which is less than my investment of Rs.2.5 Lakh.

Since I have not taken any income tax benefit on the premium paid should I pay income tax as explained above?

Amitava, its not about having claimed tax benefit or not, but about taxability of returns of the product. You have to bear the taxation.

Hello Sir, I am an NRI from Kuwait residing in Kuwait since 1997. Sir, on 26th May 2005, I had invested in SBI Life Insurance, traditional Policy- Setubandhan. It was a single premium policy. I had invested Rs. 3 Lakhs in it for the term of 10 years. It got matured on 26th May 2015. It was funded from my NRE account at Mangalore. It was 5% guaranteed addition plan. Nothing is transparent. But after asking several times i came to know that it has become 4.5 lakhs altogether now.

Now, when the maturity proceeds did not reach my NRE account, on inquiry i was told that I have to submit 10 F form for it. Then I get a new mail saying that I need to submit TRC (Tax Residency Certificate) from Kuwait to lower the tax burden. As it is difficult to get here and we need to spend lot of time in the government offices, which is not feasible, as we reach to work on time here, I said go ahead with tax cut as i knew that on submission of PAN card ( which was given to them in the month of march-2015 itself), the tax deduction will be 2% on the addition amount that they are going to pay.

As a shock, I got a email from them saying that they are going to deduct TDS at the rate of 30.9% on the total amount payable. That is on 4.5 lakhs. Sir, please see the email posted below (on 17-06-2015):

Net payable before TDS – Rs. 4,50,000/-

Less- TDS @30.9% – Rs. 45779/- (TDS will be calculated on Maturity less Premium billed i.e. on 148152/-)

Approx. Net Payable after TDS – Rs. 4,04,221/-

Thanks & Regards,

Sonam Vohra

Dy Manager-Operations

Tel : +91 80 25944981 / 84

SBI Life Insurance Co.Ltd

No 23, 2nd Floor, Yamuna Complex,

7th Cross, Malleshwaram, Bangalore 560003

Then i replied saying that you cannot tax the capital of 3 lakhs. I got another mail today (on 18-06-2015):

Pls find revised.

Net payable before TDS – Rs. 4,50,000/-

Less- TDS @30.9% – Rs. 45779/- (TDS will be calculated on Maturity lessPremium billed i.e. on 148152/-)

Approx. Net Payable after TDS – Rs. 4,04,221/-

Sir, I did not give them a go green signal for the crediting of the same. I am still not understanding why are they dedcuting 30.9% on the returns. I tried in several places to find this 30.9% but i am not getting it anywhere. I all the time see it as 2% and in some places it as tax free.

Sir, I want you study my case and help me sort out the matter. The amount of around 4.5 lakhs is hanging with them since 26th of May 2015.

Sir, thanking yo in anticipation.

Waiting to hear from you eagerly.

yours,

Adwin

Adwin, in case of NRIs TDS on Life insurance proceeds would be at highest rate i.e. 30.9%.

Clause of 2% an 20% is applicable only in case of resident indians

Submitting TRC will get the deduction lower but since you are in kuwait which is NO tax country so this would not be of any help.

Hi,

Thank you so much for your very informative article and detailed responses to various queries posted. They are very helpful. I have one question about my policy as below:

I took Birla Sunlife Gold Plus plan during 2007 for 8 years and paid a premium for 3 years 10 Lakh+10000+10000 = 10, 20,000. The sum assured is 50L. The present value of the policy is around 14L. I understand that I need to pay the tax since the sum assured is less than 10 times. The policy is going to mature this year.

My question is whether I need to pay tax on the whole return of 14L or 4L after deducting the premium paid.

Thank you for your time.

Mr Krishna, as the concept of capital gain or interest doesn’t apply to insurance policies, so as far as my understanding goes tax should be applicable on the complete surrender/withdrawal proceeds.

But i think your specific policy will not be taxed, as first year premium is 10 lakh with SA of Rs 50 lakh. Other year premiums were just taken to keep the policy in continuation as per the structure of the plan.

You better get this confirmed from insurer.

Mr Manikaran,

Thank you so much for your response. Just to update you, I got the maturity amount from the insurance company and no tax is deducted at source. As you rightly mentioned, this comes under the prior 2012 plan with sum assured 5 times the premium paid. Thank you once again for your help.

That’s great.

Dear Mr. M. Singal,

I am an NRI. In 2010 I have taken an Aviva New Pension Elite and paid 300.000 per year untill now (5×300.000=15 Lacs) The value at the moment is around 1800000.

The policy was for ten years, but after 5 payments I can surrender without charges.

I did that, asked for surender, but they only credited into my NRE account INR1235889

There is a big difference on this ammount, I asked them and and the only answer was …”it is for TDS”

I don´t have any income in India, even I dont have any NRO account…is this correct ??

(the fund allocated was Pension Index Fund II )

Thanking you in advance, please help me this matter.

Rgds

NIshal Gokaldas

Mr Nishal, as your policy was a pension policy thus there might not any insurance cover against your premium. In case of NRIs, TDS percentage is highest i.e.@30%.

Whatever amount you get from this policy will be treated as your Indian Income. Now as the amount itself is more than 10 lakh so your total income in India automatically comes under 30% tax bracket.

But still as you don’t have any other income in india, you should file Income tax return and take benefit of the tax slabs. You will definitely be eligible for some refund.

You could have planned the withdrawal by withdrawing Rs 4.50 lakh in a year and invest Rs 1.50 lakh in section 80C instruments to reduce your tax outgo. But now when the damage has already happened so there’s only one solution of filing return and claim some refund.

Dear Mr. M. Singal,

Thank you very much for y/reply.

Can you please let me know how and when I have to fill the refund ?

Who do I have to contact?

Is this TDS 30% started now ? Because 2/3 years ago I had the same situation and after I surended they gave me all amount.

Thank you once again.

Rgds

Nishal

You don’t seem to have gone through my article. Yes TDS deduction has started from October 2014.

If you had surrendered your policy before 31st March 2015, then you can file your IT return this year. but if surrendered after 31st march 2015 then you have to file return next year. Contact Chartered accountant or tax return preparer for this.

Thank you very much!!

Dear Mr. M. Singal,

I am an NRI. In 2010 I have taken an Aviva New Pension Elite and paid 300.000 per year untill now (5×300.000=15 Lacs) The value at the moment is around 1800000.

The policy was for ten years, but after 5 payments I can surrender without charges.

I did that, asked for surender, but they only credited into my NRE account INR1235889

There is a big difference on this ammount, I asked them and and the only answer was …”it is for TDS”

I don´t have any income in India, even I dont have any NRO account…is this correct ??

(the fund allocated was Pension Index Fund II ).

Thanking you in advance, please help me this matter.

Rgds

NIshal Gokaldas

Respected sir..

Ur messages are very informative and useful. Thanks a lot for ur guidance..

I have a query regarding life insurance policy. I hav a policy in kotak life insurance n a policy on fr my father in icici and a policy on my mother in bajaj life insurance. Although d policies are on different names, being elder son I’m paying the premiums annually. I hav got a call in Apr 15 saying that I hav got bonus on both icici and bajaj policies and told to claim d bonus asap. They told that I can get mingle up all d three policies and get d money on my name as I’m d money payer. As I want to close all d three policies n get d money I agreed fr d same. That agent told me pay 70000 for security amount, to create agent code, ITR and income tax certificate. They sent me an agent from exide life insurance. I gave dem a cheque of 70000 on exide life insr. They gave me date of releasing amount is 29 Apr 15 And d amount is Rs 4,07100/-. Aftr days dey said dat d kotak amount also can b included in dis as d policy is on my name. They told dat d total amt would b Rs 8,23,500/-. But I hav to pay Rs 95000/- to put it in diamond category and to make bonds which is refundable. It’s been months nw n I got a call again intimating dat d money has to be released but I hav to pay TDS which is refundable too… The total matured money nw is around Rs 12,00,000/-. And d payable TDS would be Rs 2,15,000/- on d name of BSLI service.

The question is is it psbl to merge d policies like dis.. If at all possible is there any thing lyk bonus??. Wt is d procedure actually.. Is there any fraud in this?? From where will i get my insurance amt? What is d regulatory authority?? Wt is diamond category?? Pls guide me in dis regard. It would be very helpful fr me.

Thanks a lot

Yes this is a Fraud.

Policies cannot be merged like this. From your query i can figure out is that you have paid Rs 70000 by cheque and till date you have not got any amount /bonus/or anything back. and these guys time and again calling you by increasing the bonus amount and ask for more money from you.

If this is the case…better to contact POLICE.

i want to know that i invested signal premim in lic plan no..191/10/1 on 2005 now i surrender then tds would be deduct or not?? ples reply me

thanx

Sir:

I had a Lifestage pension plan of IPRULIFE taken in 2008/9. Premiums 3 lac per annum. Paid for 3 years and stopped. I surrendered in Jan 2015. TDS was not deducted from the value.. Does this mean the surrender proceeds is tax free or I have to pay tax only on the profits?( excl amount of premium paid by me)

I have bought a SBI Life policy in 2009. The annual premium was 100000/ and the sum assured was rs 3,75,000/=. Now the policy matured in JUne 2015 and I got Rs 4,25,000/ as maturity proceeds less than the premium I have paid (Rs 1,00,000 per year for 5 years= Rs 5,00,000/). They have deducted Rs 8500/ TDS also. I think, since the maturity value is less than the sum assured I should not be taxed. Is it correct? KIndly respond

Amit, Life insurance returns doesn’t come under capital gains, neither does it earn any interest, so whatever proceeds you get from your policy will be treated as income.

If Policy has the adequate sum assured to make it non taxable u/s 10(10d) then its ok, otherwise complete proceeds would be taxable, even if it is less than what was paid. In your case complete 4.25 lakh is taxable.

Thankyou Sir, for your response which is quite clear. One small doubt is remaining As I am coming in 30% tax bracket that means have I to show the maturity proceeds of SBI life of Rs 4,25,000/ as my income in FY 2014-15 and pay tax @ of 30% on Rs 4,25,000/ or 2% TDS deducted by SBI life is only my tax liability. Kindly clarify I will once again repeat my history:

I have bought a SBI Life policy in 2009. The annual premium was 100000/ and the sum assured was rs 3,75,000/=. Now the policy matured in JUne 2015 and I got Rs 4,25,000/ as maturity proceeds less than the premium I have paid (Rs 1,00,000 per year for 5 years= Rs 5,00,000/). They have deducted Rs 8500/ TDS also.

Hello Mr.Singhal,

I have been paying ULIP premiums in three different policies since 2007 for 5 years or more. Since 2010 I am living and working abroad. All the insurance premium so far were paid from my indian earnings. Since the sum assured is very less or nil, the TDS is surely applicable. If I surrender the policies now, the TDS applicable will be as a resident indian or NRI? Also, how shall I receive this amount? In my NRO account, or a joint resident SB account with my wife who is a resident Indian unlike me. Will this make any difference in tax calculation?

Regards

Rejji

Hi

For the TDS quesries, if the premium paying period is oveer and owing to partial withdrawl the sum assured reduced and hence 10(10) D not met, will the withdrawl amount still be taxable?

isnt this applicable only during the premium paying period ?

I believe so. Whatever you’ve bought in the proposal and written on policy document should have to be met for TDS calculations. Partial withdrawal is the additional feature that is inbuilt in the plan and it should not impact the tax ability.

Hello Sir,

I had a pension policy taken in december 2008. My contribution towards the policy is (40000×3=120000) with zero sum assured. The fund value of the policy as on 23/7/15 is 164271 .I want to know that if i surrender the policy now is this amount i will get or not?? plz show me the calculation of charges.

Thnx in advance,

waiting for your reply

Pension policy is a taxable policy. Now if there would be TDS deduction or not, depends on the Sum assured given on your premium. Since it was bought in 2008 then the minimum SA should be 2 lakh against premium of 40k to make this policy TDS free.

But do note that TDS or no TDS your pension policy withdrawal is taxable.

Hi

My dad took bajaj pension plan in 2015 with yearly premium of 50000 and 0 sum assured. He has paid only first year premium as he need to pay 3 year to surrender policy but today we went to surrender they said as per current market we supposed to get 66880 After deducting 2500 penalty charge and 350 Service tax. Again they saying 20% tds will deduct as he didn’t have pan card but as i checked if payout less than 1 lac nd without pancard there would be no deduction pls help is tds will deduct on 66880 amount with no pancard.

TDS should not be there when policy surrender proceeds are less than Rs 1 lakh. You should mail your concern to grievance cell and check about this. But yes, as policy is not inforce then they will definitely deduct the charges.

Sorry my bad he bought policy on 2010

Sir

Request a revert. Question is specific to Birla platinum premier plan. It’s a regular 10 pay with option to clients to stop payment after 3 years.

If one withdraws in the 5 th year, SA reduces thereby not satisfying 10 10 d and hence Tds. But will the amount be taxable ?

The mandatory 3 years where premium was paid no withdrawal was done and 10 10 d was met. Insurer is not commuting anything here.

Will amount be taxed?

Hello Mr.Singhal,

I have been paying ULIP premiums in three different policies since 2007 for 5 years or more. Since 2010 I am living and working abroad. All the insurance premium so far were paid from my indian earnings. Since the sum assured is very less or nil, the TDS is surely applicable. If I surrender the policies now, the TDS applicable will be as a resident indian or NRI? Also, how shall I receive this amount? In my NRO account, or a joint resident SB account with my wife who is a resident Indian unlike me. Will this make any difference in tax calculation?

Regards

Rejji

TDS will be applicable as per your current tax status which is NRI. Hope you have got the status updated in your Insurance records. Keeping saving account is illegal for NRIs, so you have to take the proceeds in your NRO a/c.

No. I have not updated my NRI status in the ULIP policies because I had stopped paying the premiums ever since I became a tax payer abroad. Is it illegal not to update the status? Will these be scrutinized if I make a surrender request now?. Nevertheless, in a year or two from now, I will return to India for good, but I prefer to surrender now to meet some financial requirement. Your valuable suggestions are highly appreciated.

Rejji…the point is that your tax status is NRI at present, and you cannot keep Indian savings account. So you have to ask for surrender proceeds in your NRO a/c and for which you need to update your tax status as NRI in policy records. TDS will surely be deducted if applicable but if you don’t have any other income in India then you can claim refund next year by filing IT Return

I understand and thanks a ton for the clarification. But according to the article below, a resident individual holding a savings bank account, can include non-resident close relative as a joint account holder. Does this mean, the NRI can have the cheque book of the resident account he is holding with his resident relative?

Also, what is stopping him from receiving funds to this account, from any indian source?

http://articles.economictimes.indiatimes.com/2011-09-16/news/30160793_1_resident-individuals-account-eefc

Hello Manikaranji,

In 26AS, LIC showed total 242330 as amount paid/credited and 2% deducted 4846 as TDS. One of bankers have shown 18486 as credit and deducted 10% 1849 TDS. My salary income comes to 729361. Less 150000 under 80C. My question is am i liable for more tax in sese that do i need to add all above LIC + Bank deposit interest in my Other source income? In such case i will become liable for 30% of payment of Tax? Its confusing on LIC payment and how to get credit on same.

Appreciate your quick response as need to file return by Aug.31

Regards,

vijay

Deduction of 2% TDS on LIC proceeds itself says that the complete amount is taxable. You have to add Rs 242330 in your gross total income along with salary and Bank interest. Then deduct 80C savings and calculate your tax liability. Out of that deduct the TDS amount already deducted and pay the rest.

Thank you very much Sir.

Dear sir , I took the LIC policy for my children (LA) in the year of 2000 , the sum assured was 50,000. for 15 years , The half yearly premium amount was Rs 1623 and Rs. 1674 , and the same was paid till it matured in August 2015. However i was utterly surprised to see that the maturity amount in both the policies was same i.e. Rs 82 ,258/

Dis the LIC has deducted service tax and TDS on these policies , as i was relocated in different town , so the the policies and other documents i sent through post , that is why i am not aware about the deduction made by LIC.

Could you please explain me the status.

Hello Manikaran,

I have an issue with Aviva Life Insurance Saveguard policy.

I had take it in 2005 for a life cover of 1020000 and yearly premium of 102000.

I paid for 4 years and then made the policy paid up with zero life cover on 2009.

On 2015 i surrendered the policy. the maturity amount was 650000 Rs. insurance deducted a sum of 13k as TDS and gave the remaining amount to me.

Now, dont you think TDS was not applicable to my maturity amount as the premium paid was <= 10% of life cover? but aviva is citing my paid up status at the time of surrender and vouching a 2% TDS is valid.

but my tax consultant and i are voicing against this and demanding the reimbursement of 13k and also amendment to their TDS so that it gets cleared off of my Form 26S.

Please have a look at this and tell me if the TDS collected is valid..?

when i am filing my IT returns (last date is 7th sept 2015) , do i need to pay more taxes on the basis of this?

Please advice.

I m totally on your side. Paid up status should not be a reason of deducting TDS. and as per the details you shared i feel that TDS should not have been deducted. Hope this is a purely ULIP policy and not pension plan.

Hello Manikaran,

Yes, its a purely ULIP life insurance policy called Aviva Save Guard.

Thanks for your advice.

Could you please advice me also on what action i can take up with Aviva? Since they have already paid TDS of 2%.. i have requested for amendment and reimburse the money. But moreoever, while filing returns, Income Tax may come back for enquiry if they scrutinize my Form 26s. What action should i need to take when that happens?

Thank you for a timely reply !!

Chandan.

Dear Manikaran,

Please find the reply from Aviva.

——–

This is with the reference to your concerns raised with us regarding the above mentioned policy.

We have noted your concerns with respect to your policy. However, we wish to clarify that upon conversion of your policy into a paid up policy with zero sum assured, the same became non-compliant to Sec 10(10D) of the Income Tax Act.

A policy becomes non-compliant to Sec 10(10D) if at any stage the sum assured in the policy falls below the minimum multiplier of the annual premium as stipulated. In this policy, the applicable multiplier is 5 times of the annual premium and upon reduction of the sum assured to zero in Mar’09, the policy became non-compliant to Sec 10(10D).

Upon surrender of the policy in Jan’15 and as per current tax laws, TDS was applicable @ 2% on the date of the payout request. We wish to assure you that TDS has been correctly deducted prior to the payout as per applicable tax laws. The TDS certificate has subsequently been issued by the authorities and it has been shared with you. We once again request you to seek advise from your tax consultant regarding refund of the same from the authorities if applicable.

——

Is there something i can fight these folks who have charged this TDS?

Should i need to go ahead and file my returns and have to pay a 28% (30- 2%) of total amount that was paid by Aviva as part of surrender of my policy? That would be a huge amount of Rs.190000 Rs as Tax??

Appreciate your analysis and advice.

Thank you,

Chandan

Chandan, what aviva has replied is logical. I confirmed from some of my planner friends and they agree with aviva’answer. If at the time of withdrawal, policy is not satisfying the condition of 10(10)d which is minimum times of sum assured to premium then the policy will be termed as Taxable. and the same happened in your case which has made your policy taxable. Now the complete surrender proceeds have become taxable.

However i still feel that you should discuss this thing with your CA or tax lawyer and take their point of view too…and then act accordingly.

I am an avid reader of your blog and find it very interesting and knowledgeable. I want to ask the following questions for your experts advice :

I have two LIC policies in my name : LIC Jeevan Anand (issued in August 2006 and maturing in August 2021) and second, LIC Jeevan Saral (issued in November 2009 and maturing in November 2024).

I want to surrender these two policies.

I want to know the tax implications :

1. Will the surrender value be taxable in my hands.

2. If yes, will the entire surrender value be treated as income in my hands and taxed accordingly. Since the surrender value is less than the sum of premiums paid by me so far, therefore, there is a loss occurring to me. How this loss will be treated – either in the form of loss of income for the current year or a capital gain loss.

3. Will the 80-C benefits claimed in earlier years by me, will have to be reversed, if any.

I would be greatly thank full if you could answer my above queries. And reply to me by email in addition to your normal system of publishing the query and reply it on your website/blog.

Thanks Mr Garg for reading an appreciating my articles. Pls find my replies in the same sequence of questions:

1. As both your policies were issued before April 2012, so there has to be sum assured of atleast 5 times of Annual Premium payment. If your policies have required minimum sum assured and these are not pension plans and the policies are still inforce ,then surrender proceeds would not be taxable

2. If the surrender value was taxable, then the total surrender proceeds would be added in your income. Even if it is less than the Premium paid and thus at Loss. Whatever you get would be treated as you income.

3.80C benefits would have got reversed if your surrender of policies were falling with in first 5 years of policy continuance.

Hope your doubts are clear now.

Hello Manikaran Sir,

Your blog is very helpful and will clear all doubt about the ULIP plan. Thanks for your response and time.

My issue is slightly different than all above question.

I have bought the ICICI prudential plan in 2006 with Rs 50000 yearly premium and sum assured as 250000. so this coveres 10 (10D) benefit,

However i have done the partial withdraw during year 2009 and ICICI had reduced the sum assured to 1,00,000 Rs.

I have continue to pay the premium as 50000 per year till June 2015. I have surrender the policy and got the 443000 Rs with 2% TDS deduction.

Based on your above reply I think this total surrender value must be taxable and i should add this in my total income. I am correct on this or should i consult any CA for this?

Thanks in advance for your valuable reply.

Hello Harshad

Thanks for reading and liking my articles.

Yes. The total surrender proceeds would be taxable and has to be added in your income. You can gauge this from the fact that 2% TDS was deducted on the complete proceeds and not only of the gain amount.

Hello Sir,

I have bought a single premium Policy in 2011, IndiaFirst SmartSave from my NRE savings account, single premium amount 15 lac and life insurance offered 1.25 times of single premium. It is debt linked plan and its current value is around 21 lac. Maturity will be in 2026. I received the letter from them that as per new ITAX laws the maturity proceeds or full/partial surrenders will be subject to TDS of 30.9% rate.

Now, in case before 2026, I return back to India and become Resident Indian and do full surrender or get maturity in 2026 as resident Indian then what will be TDS applicable rates? Once I return back forever, do I need to inform Insurance company that I have returned back to India forever and change my status from NRI to Resident in their records?

Dear Sir,

I had purchased Bajaj Allianz Max Advantage Insurance Plan (Equity Index Fund II) in January 2011. Annual premium was R25,000 and the sum assured was R2.5 Lakh. I paid first three premiums but could not pay the last two premium. I also availed tax deduction u/s 80C for the three premiums paid. After the non payment of premium, fund was transferred to discontinued fund. As of now, the ULIP is out of lock in period of five years and the discontinued fund value is R90,800. What will be the tax implication if I surrender and get the proceeds? will it be taxable or tax-free?

Sunil, after the fund gets transferred to discontinued fund, the insurance cover lapses. Now if you surrender the policy, company will deduct TDS and also the complete surrender proceeds would become taxable. The best thing to avoid tax is to pay the balance premium and reactivate the policy with all the benefits and 10 times of SA…and then surrender.

But for this you have to first compare the deduction in shape of tax and deduction of charges in reactivating the policy and then take final decision.

i have bought a bima bachat policy with sum assured 40000 and single premium 25333 now sb is due with rs 3000 whether tax deducted on this amount

Yes. Your policy proceeds would be taxable

Respected Mr Singal,

I have two small issues for which I require your guidance.

(1) I had bought LIC endowment policy with SA Rs.50,000/- and yearly premium of Rs.2520/- in 1995, which is maturing now. Will it cover under 10 10(D) or not? or How will it be taxable?

(2) I had also purchased ULIP from LIC (Wealth Plus) in 2005 for Rs.45,000/- (single premium). I have surrendered the same in October, and have received Rs.51,000/-. How will this be taxable? Since it is ULIP, will it be treated as long term capital gain and becomes tax free or have I to show difference of Rs.6,000/- as Income?

Please oblige, thanks

2) if it is taxable then complete 51000 will be added in your total income

Repected Mr Singal,

I have two small issues for which I require your guidance.

(1) I had bought LIC endowment policy in 1995 with SA Rs.50,000/- and yearly premium Rs. 2,520/-, which is maturing now. Will the maturity value cover under 10-10(D)? or, will have i to show as income?

(2) I had also bought LIC- Wealth Plus (ULIP) policy in 2005 for Rs.45,000/- single premium. I have surrendered the same in Oct’15 and got the Value of Rs.51,000/-. Will the gain be treated as Long Term Capital Gain and Exempt from Taxable income? or, entire Rs.51,000/- will be considered as income as chargeable to tax?

Please oblige with your advise.

Hello Naresh.

1) This policy covers the condition of 10(10d) of minimum 5 times of SA, so the maturity amount should be tax free. Though you have to show this in your IT return under tax free income.

2) As the policy was single premium you need to check the Sum assured attached. If it was Rs 2.25 lakh or more, then you need not to worry otherwise if it was less then this complete Rs 51000 will be added in your income and taxed as per IT slabs. Returns from Insurance policies if taxable then comes under “Other Income” category and will get added in your total income.

Btw, was there any TDS deducted on maturity amount of wealth plus?

Dear Mr. singal

Thanks and obliged for the queries answered.

No TDS was deducted from the maturity value. Hence, should we take it to Capital Gain?

Check out the sum assured then. If it was 5 times of premium then NO tax to be paid, otherwise add the complete proceeds to your income.

Sir,

i buy max life monthly income advantage plan 12 days ago. Premium amount is 99999.97. sum assured is 1422677. Monthly income benefit is 11856.00 for ten years after payment of all premiums.Premiun payment term is 12 years.After 22 years non garanted bonus etc. will be given . T.D.S. will be deducted @ 2%.Please answer me whether the monthly income benefit and maturiy benefit both are tax free under section 10/10d.

Please oblige, thanks

Respected sir

I buy LIC of INDIA Endowment Plus Rs. 100000 sicne 2010. Now I want to sureender my policy . My policy Fund Value is 143000 I have no pan card . How many tax deduct in my total amount

It depends on your Insurance Sum assured. If you have at least 5 times of premium amount as insurance cover then there won’t be any tax deduction, but if its not then with no PAN card TDS deduction would be 20% of total amount.

Dear Mr Singal,

I bought a LIC Market Plus 1 ULIP policy on Nov 2008 with a monthly premium of Rs 3500/-. This policy was attached with a Life cover of Rs 1,00,000/- (all guided

rather misguided by the agent). I continued this policy until June 2015 and then surrendered as the fund was not doing well (it was less than the total premium paid).

The surrender value was around 276350/- . LIC deduced 2% as TDS since my PAN was registered. My question is

Q. Will the surrender value be fully taxable this year ? even if I didn’t claim this in 80C earlier years ?

a. If yes, then I will end up paying double tax on the same income (earlier years and this year). I even not made any profit on this.

b. If not then how (which section) to declare this income. My 26AS already reflects this income.

Thanks in advance for your comments.

Yes, Mr. Partha, the complete surrender value is taxable. You would have observed that 2% was deducted on your total surrender amount. Even if you have made any profit on this or not, you have to pay tax on total amount. Technically you may say it double taxation only, but this is how insurance product works

I have a policy which is not exempted u/s 10(10D) of the Income tax Act.The policy is matured on 26/07/2015. I have received Rs. 3469200/- (basic amount rs. 3029200/- and bonus Rs. 440000/-. Tax has been deducted Rs. 69384/-. I have no other income. Please inform me whether Rs. 3469200/- will be treated as my total income for which have I pay Income Tax after deducting Rs. 69384/- TDS.?

If premium paid in excess of 20 % or 10 % as the case may be is not allowed under 80C , then on maturity or surrender can we claim deduction for not allowed part of premium

I am a student i am not a income tax payer On 10/jan/2015 we made a fixed deposit ( 500000 ) in hdfc bank it was matured on 11/Jan/2016 but I have submitted 15g form once’s in FD period at the time of maturity from interest TDS was dedcted from interest. Is it possible to get back that amount if yes please provide information and process.

Thank you

File the tax return and if your tax payable is less than the TDS amount then you can claim back the tax dedcuted.

Sir,

My question is that can I claim refund of TDS deducted under section 194DA .

My income is exempted under section 10 (26) of IT Act 1961 but LICI has deducted TDS @ 2% on maturity amount.

If i can claim refund of entire tds amount , then how to show in income tax return?

while filing return you will calculate the self assessment tax and also mention the tax paid through TDS or Advance tax. If Tax paid is higher then tax deductible then you will get the refund of amount.

Sir,

I had taken a Max Life Smart Assure ULIP policy with monthly premium of Rs. 2000 (from NRE account) for 20 years in June 2009. Since ULIP are not giving good returns I surrendered the policy in Dec 2015. After surrender charges the final amount payable was about 1,80,570.46. I did fill the NRI declaration form but no TDS was deducted. But the bank refused to credit the amount to my NRE account through NEFT. So MaxLife issued me a cheque which I deposited in the account but ICICI Bank refused to credit it and sent me a letter saying ” NRE Source of fund proof required”. What do I have to do as the bank & insurance company are giving conflicting answers. Your help would be much appreciated. Thanks

If you had taken a policy as NRI, then definitely at the time of policy buying uou must have indicated somewhere your residential status, and Insurance company must be knowing that you are paying through NRE account.

Bank is right in refusing the credit of funds, as long as it is not sure that money invested, was paid through NRE account. You need to have a letter from Insurance company stating that premium was paid through NRE account

Dear Sir, I am an NRE(UK resident). My Query is that I have invested 60 Lakh for 3 years in Regular Premium Pension Plan(no sum assured) and current value is 2.4 cr. I have taken policy in March-2010 so if I surrender policy after seven years will I get any advantage of tax free years for saving tax on profit earnings from my policy. Since I don’t have any other income in India. Currently company is deducting TDS on profits.

Mitesh, Pension plan has always been a taxable product. So if you withdraw 2.4 cr now, the full amount will be treated as your income in India, and thus will be taxed accordingly. Though Insurance company should deduct TDS on it, but even if it doesn’t, then legally you are liable to pay tax on it

Hello

I am an NRI. A part of my equity mutual fund investments (invested as NRI) I had to redeem within an year which attracted TDS on short term gain. I do not have any other source of income in India. Can I claim this amount, by filing tax returns?

BR

Rejish

Yes Rejish, you can claim the TDS by filing tax returns

According to the details mentioned in sbi website (given below), there are no exemptions for “Short Term Capital Gains” for NRIs. Am I missing something? https://www.onlinesbi.com/nri/sbinri_faq_tax.html

BR

Rejish

See taxation of capital gains are same for NRIs and Resident Individuals. STCG in equity is taxable at 15% to both, and LTCG is tax free. NRIs’ gains are subject to TDS. But if on self assessment at the end of year, one finds that there’s no Income tax liability on him, then the assesee can claim back the TDS deducted

I misinterpreted it. Thanks for the clarification Mr. Singal. As usual your advises have been very helpful. I filed my returns today.

PLEASE ANS. ME ABOUT WHAT AMT. WILL BE TAXABLE IN CASE OF LIC PREMATURED IN THE FY 2014-15

Pls share your policy details

Dear Mr. Singal,

I am an NRI living in UAE. Yesterday I surrendered my Life Stage Pension Policy of ICICI Pru Life (No Sum Assured) after 7 years (paid only for 3 years Rs.1 lakh premium per annum) Total surrender value after deduction of surrender fee comes to Rs.4,66,471/-. The person at iciciprulife said that TDS will be deducted at 30.9% of profit i.e. Rs.51,439/- (on profit of 1,66,471/-) and I should claim it by filing tax return and there is no other way. He has given me a written note of the calculation. The amount I will be getting is Rs.4,15,032/- as per his note. My PAN is already registered with them as well as I gave a copy yesterday also. Is it correct? or is it 2% of total value?

Regards and awaiting you reply.

Mr Dsouza, i am not sure if the ipru person told you the correct thing or not. What i know is that Pension Policy is 100% taxable policy and thus the complete surrender proceeds should be taxable, and not only the gain.

TDS rate in case of NRIs is 30.9%, so as per me the deduction should be 30.9% on your fund value. Now all this thing will get cleared out when you receive the amount in your account.( Please do keep me posted)

In some of the cases, i have seen ICICI did not deduct any TDS, i don’t know why. But that doesn’t mean the policy becomes tax free. It is still taxable and taxes needs to be filed seperately.

Dear Mr. Singal, I have received an amount of Rs.415,227.79 credited in my bank a/c, therefore it is sure the TDS deducted on profit of Rs.1,66,471/-. I have not received any documents as yet and will know exact amount and deduction from that.

Regards,

Roque Dsouza

Hello Mr Dsouza. I asked few of my fellow planners on your query. One thing i got to know is that in Pension plan there is no TDS applicable under section 194., But still as it is fully taxable policy so in case of NRIs companies do deduct TDS.

In your case, even they are not sure why TDS was applied only on the gain amount. As per tax laws pension plans are completely taxable on surrender. Now as far as my understanding goes you need to show the complete proceeds as your income and file tax accordingly. Still its better to consult some Tax expert, or ask the taxation laws from ICICI pru people only. Yes…this would be much better. Write down mail to the customer care and ask for the taxability of your policy

Hello Mr. Singal, I had filed the return through Chartered Accountant showing only profit amount (amount on which TDS deducted) as per the TDS certificate. Assessed as per my computation and full refund received with interest and assessment order also received.

This might be useful for you to advise to other NRI’s who seek your advice.

Regards

Roque Dsouza

Thanks Mr Dsouza

Dear Manikaran ji,

thank a lot for sharing such a typical part of law in such a simple and self explaining manner.

please make one more thing clear. if a policy (be it one time premium, or be it ULIP or be it regular policy) fulfills 10 times sum assured condition, then after how many years, the policy should be surrendered to avoid any tax on surrender value.

i have heard that regular policy should be invested for a minimum term of two years and ULIP/single premium policy should be invested for at least 5 year (surrendering before this period will invite taxability).

please clarify

Thanks Piyush for liking my article.

See, to make the surrender proceeds tax free you just need to be sure that policy sum assured should atleast be 10 times of the premium and this should be the case even at the time of surrender. Now there’s no holding period defined as such. This comes under policy features, if the policy allows you to surrender the plan after 2 years, with no surrender charges then whatever you get will be tax free. 2y/5y terms which you have mentioned is for making the policy eligible for surrender. Just go through the policy discontinuation and surrender clause in your policy document.

One thing you should know is that if you have taken any LI policy for tax benefit u/s 80C, then 5 year holding is must., otherwise all benefits claimed through this policy u/s 80C will get reversed.

sir,

i have taken SBI life policy single premium plan

premium is 1,70,000/-.

basic sum assured is 1.25 time i.e. 2,12,500/-

SBI has invested this 1.7 lacs in a fund and allotted me 7379 units of that fund.

i can claim 21,250/- u/s 80C. (being 10% of sum assured)

but at the time of maturity get the maturity if i get 3 lacs (being NAV) whether whole three lacs will be taxable or the income portion 120000 (300000 minus 170000) will be taxable.

thank you in anticipation

Hi Sir,

I am filling my return as NRI, I took SBI Life Unit Plus III Pension policy for 6 lakhs rs (without insurance cover ) on 10-AUG-2010 . I want to surrender it now. Kindly tell TDS will be 30.9% high and if so will I able to claim it back at the time of filling the return . Please note that at the time of filling the return for financial year 2010-11 I didn’t took the benefit of section 80 .

Shishir, being an NRI, your surrender proceeds would surely be subjected to TDS. and Yes, you can claim it back by filing ITR.

Dear Sir

One of my client got a payment from lic as a nominee on the death of his son. lic deducted tds u/s 194DA @ 2%.

will this amount be taxable in my client’s hand.

sir my father is going to take a ULIP plan for term- 10 years ,ppt-5 years , His age is 58 years,

premium is -200000 per year and sum assured is -1400000. if he withdrawal after six years then maturity will be taxable or tax free .

Maturity will be taxable, as the SA is not 10 times of Premium. To make the maturity proceeds tax free in this case Sum assured should be Rs 20 lakh.

Dear Sir,

I am NRI and do not have income in india so do not file returns. I have bought ICIC Prudential ULIP insurance plan in 2004. sum assured is 300000 and yearly premium is 100000. I have paid 2 extra premiums making it 500000. Now if I want to surrender the policy will have to pay 30.9% TDS? will it be on full amount? or only the bonus accrued? Can I withdraw only principal amount and save taxes?

Would appreciate your response.

Thanks.

TDS will be deducted on full amount. There’s no way you can withdraw the principal, as value would be calculated in terms of Units, and now every unit has some portion of growth in it.

In this case, there seems to be an anomaly. There was no tax exemption claimed from the premium paid to Insurance company in earlier years. If the entire surrender/maturity value (principal plus increased value of units) it becomes a case of taxing the principal amount twice. This becomes important when there are cases of single premium policies. While the insurance company may deduct 2% from the entire surrender/maturity value, is there a way to claim exemption for the principal amount while filing the return. Would appreciate your considered views on this.

No. It doesn’t matter if you have claimed any tax benefit at the time of investment, what matters is if the policy is taxable at the time of surrender or not. If it is taxable, then complete proceeds would be taxable. In Insurance there’s no concept of Interest or capital gain, where principal needs to be taken into consideration.

This is not correct. We are not talking about insurance here, but of income tax. In the income tax there is a principle of not taxing the same income twice. Suppose the premium paid by this gentleman is already taxed earlier, why should it be subjected to tax again ! Would request you to advice whether one can deduct the premium amount from the total surrender while filing the return. Its true the insurance company may deduct tax on the entire surrender value, but it is possible to adjust it while filing the return. Request you to clarify whether I am correct on this please.

I don’t think so. To my understanding the complete proceeds would be taxable. This is the beauty of Insurance policies, either nothing is taxable if policies falls in 10(10d) or everything is taxable.

Dear Sirs

I am a NRI, my SBI Life Unit Plus Super LP is completing its 5 years soon and i am planning to surrender it as soon as it completes 5th year as the return isn’t what i was told it will be.

My question is whether the return amount (Rs 599900) will be taxable via TDS, if yes what would be the tax rate?

Thank you

BW

Samy

If you have bought policy before 2012 and SA of the policy is 5 times of Premium, then there would not be any TDS deduction , provided this is not a pension plan. Else 30.9% of TDS will be deducted.

Dear Mr. Manikaran,

Thank you very much for your illustrative responses on the 2014 amendment to section 10 (10D) .

However i have not seen any topic of taxation on return of survioval benefit from LIC Beema Bachat policy.

I purchased the single premium LIC policy in March 2013 for some assured Rs. 1,000,000.

Recently LIC paid me Rs 147000 as survival benefit ( 15 % of sum assured after 3 years) after deducting 2 % Income tax.

Am i right in assuming that the full benefit amount is to be treated as my income and added to my total income for this assessment year?

How is the final maturity amount will be taxed?

Thanks in advance for your replies.

Best Regards

Yes you are right. If the sum assured in the Policy is not 10 times of Premium paid, as in your case, then whatever and whenever you get any survival or maturity benefit, full amount will be added in your that year’s income and taxed accordingly.

query pertaining to ICICI Pru Lifetime Super Pension & Premier Life Pension , Policy held with ICICI Prudential Life Insurance Company Limited.

The policy was issued on February 2, 2008 and 23, 2009 along with the first premium deposit for the said policies.

I want to surrender the policy. As per the product norms surrender Value is payable after the policy has completed 3 years and the premium have been paid for 3 yrs.

One policy is full NRI funds, second policy 1/4 is NRO funds. ICICI pru

First policy deducted TDS 30%

Premium paid 30lac in 2008 and 2011 for first policy deducted TDS and are paying amt Rs36,12,750.

Certificate stated zero TDS

They also stated they there is no double taxation treaty between India and Uk?

Premium paid for 3,80,000 NRE account for second policy 2009 and 2lac demand draft from ICICI bank 2013 for which we are able to find the source, I am ready to to say it’s NRO just bcz the banks are not cooperating in giving information.

Amt yet to pay Rs 894146 by ICICI prulife

I live abroad since 1998/9 till date.

Since a April 2016 am trying to get the surrender Amt. but either ICICI has not submitted repatriation letter or are unsuccessful in NEFTS which was my first request.

TDS has been deducted but letter issued states 0.00 is this ethically right?

Every day I spend time on phone or email but in vain. Hardly get responses. Their greivece dept is as good as dead.

Is Icici right in deducting tax for NRI funds if yes are they right to state zero.?

Double taxation treaty with Uk?

If ICICI bank is not able to find source of fund what are my options?

Thanks for reading and if you are able to respond.

Regards

Dear Sir,

I have few queries pertaining to ICICI Pru Lifetime Super Pension & Premier Life Pension , Policy held with ICICI Prudential Life Insurance Company Limited.

The policy was issued on February 2, 2008 and 23, 2009 along with the first premium deposit for the said policies.

I want to surrender the policy. As per the product norms surrender Value is payable after the policy has completed 3 years and the premium have been paid for 3 yrs.

One policy is full NRI funds, second policy 1/4 is NRO funds. ICICI pru

First policy deducted TDS 30percent life time super pension

Premium paid 30lac in 2008 and 2011 for first policy deducted TDS and are paying amt Rs36,12,750.

Certificate stated zero TDS

Premium paid for 5lac second policy 2009 and 2013 for second policy a sum was paid by DEmand draft for which we are able to find the sorce but are ready to to say it’s NRO just bcz the banks are not cooperating in giving information.

Amt yet to pay Rs 894146.

I live abroad since 1998/9 till date.

Since a month am trying to get the surrender Amt. but either ICICI has not submitted repatriation letter or are unsuccessful in NEFTS which was my first request.

TDS has been deducted but letter issued states 0.00 is this ethically right?

Every day I spend time on phone or email but in vain. Hardly get responses. Their grevience dept is as good as dead.

Is Icici right in deducting tax for NRI funds if yes are they right to state zero.

They also stated there is no double taxation treaty between uk and India, is this right?

What’s happens if am not able to find the source for the demand draft ICICI generated?

Thanks for reading and if you are able to respond.

Regards

Sir,

I am an Indian and have a Bajaj Allianz Max Gain-1 highest NAV policy started in Dec 2009 Maturity is on Dec 2019. Sum assured is 5,00,000. I have paid 7 years and policy is still in force.

The current fund value is ~8,30,000.

I want to surrender this policy. I have following questions

1. Will this amount 8,30,000 be tax free since i am closing it before maturity?.

2. Or will there be deduction of 2% as TDS under 194DA ?.

Thanks in advance for your replies.

Best Regards -DJ

You have not mentioned the annual premium amount. If it is Rs 100000 or less, and the policy is inforce then it should not deduct any TDS on surrender.

I am an NRI. I have recently surrendered a policy with Aviva Life Insurance. They have deducted TDS @ 30.9% on the full surrender value. Surrender value is 10,46,609 and TDS deduction 3,26,875/=

How can I get the TDS amount back and is there any interest associated with the payment.

Thanks.

You need to file ITR in India to claim the TDS amount back. However you may not get the complete amount back, since if TDS has been deducted from policy proceeds then it shows that proceeds are taxable. In Insurance there is no concept of interest or capital gain, so whatever is the surrender value would be the Taxable income generated. So in your case Rs 10.46 lakh would be considered as the income in a financial year( assuming there’s no other income). So now you will have to calculate taxes as per the IT slabs and can claim back whatever have paid extra.

Hello Sir :

I live in US from past 20 yrs as US citizen. I invested in the ICICI Prudential Life Policy in June 2010 from hyderabad. Paid premium of Rs 9 lakh and now it is time to surrender. I gained Rs 3 lakh on the Policy with the total current value now being Rs 12 lakh on the policy. So can u please confirm if my profit amount is taxed at the rate 30.9 % ?. I have never paid taxes in India and do not have an PAN card as i pay the taxes in US. I just applied for the PAN card just incase. Can you please confirm if i have to pay the taxes as an NRI ?.

Will the amount would be given to me in full value of 12 Lakh and do i have to file the taxes separate. I know if i dont pay it in India i do have to report it in US.

Can you please kindly Clarify !

Thank you So much ..Yakoob.