Rahul Singh has a well-diversified investment portfolio. He has followed financial planning principles to the core, and has always invested with a goal in mind. His next big goal: funding his Child education expenses. He has one son Vihaan and he wants to plan for his higher education.

Singh has a public provident fund (PPF) account under his guardianship in the name of Vihaan, specifically mapped towards his education goal. Singh has been saving Rs. 1.50 lakhs every year in this PPF account to save tax but wants to achieve Vihaan’s higher education goal partly from this corpus. He does not want to touch his equity investment till retirement as it has given much better returns than PPF.

Singh figures he needs Rs. 26 lakh for Vihaan’s education – Rs 4 lakh each for the first four years of graduation and Rs 5 lakh each for the next two years of post-graduation. But he is unsure where to invest the Rs 26 lakh, to account for education inflation during this phase. He is familiar with wealth accumulation strategies which are frequently featured in newspapers, financial blogs and TV shows but is clueless about the plan of action to follow during the distribution phase – the period post accumulation.

Should he maintain a status quo on his PPF investment or withdraw money and invest elsewhere to meet his child education expenses?

In technical terms, we can say that Singh is looking for a money distribution strategy. Different distribution strategies are used when the money requirement is spread over more than one year. ( Also Read: Retirement distribution strategy – Bucketing approach)

As Vihaan’s education is spread across six years and Singh wants to plan three years in advance, he has eight to nine years before him. This requires a definite strategy, wherein education inflation is managed with a low tax burden on the investor.

Let’s see what distribution strategies Singh can opt for his child education expenses.

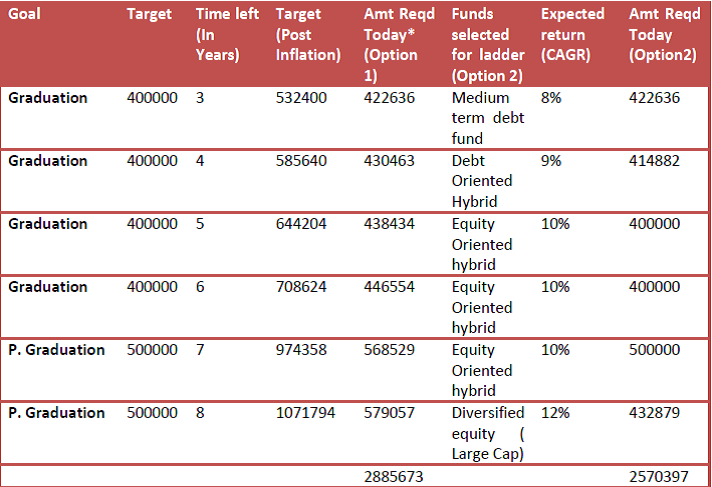

Before he begins, Singh has to consider two things – education inflation and taxation on returns. Assuming 10 per cent per annum education inflation, Singh has two options to meet his goal.

One, extend his PPF for a block of another five years, with or without contribution (his PPF investment has already completed 15 years). PPF has a provision of continuing the same account without any further contribution, with one withdrawal of any amount per year from it. For “with contribution” accounts, withdrawal up to 60 percent of the balance at the beginning of each extended period is permitted.

In this way, Singh can keep earning tax-free income yet take care of the education inflation. But this approach has two hitches. One, since the PPF is generating 8 per cent plus returns and inflation rate is at 10 percent plus, the approach may require more funding, which means Singh will have to stretch his budget.

Singh has a second option to manage his child education expenses. He can employ a laddering strategy with mutual funds, wherein the total investment amount is spread into a number of funds, to be redeemed one fund at a time to pay for that year’s education expenses. This distribution strategy is generally used in fixed income investments where bonds of different maturities and interest rates get purchased to manage the interest rates and reinvestment risk and to maintain a steady cash flow.

Since Singh’s requirement is spread across several years and has to take into account inflation and taxation, mutual fund laddering may suit him best. His choice of funds can range from the very short-term liquid funds to mid-cap equity funds, which are meant to be held for a long term.

To create a ladder in this specific case, where the first installment is due after three years and last eight years, Singh can invest in a combination of medium-term bond fund, debt oriented and equity-oriented hybrid funds as well as a large cap equity fund.

Child education expenses – Mutual funds laddering distribution strategy

To manage the taxation part, he can invest in medium term bond and debt-oriented hybrid fund in the name of Vihaan. By doing so, the taxation will fall on Vihaan at the time of maturity or redemption as he would have become a major by then. Equity-oriented hybrid and pure equity funds generate tax-free returns. (Check the table above)

Laddering through mutual funds to manage child education expenses may require less funding overall, as some part of the allocation will go into equity-oriented funds which has the potential to deliver much better returns in the long-term. Even in debt funds, good returns are expected as interest rates are expected to fall in future, benefiting bond funds.

This distribution strategy, though, may have to be constantly reviewed, to allow for the necessary switching and redemption, considering the volatile nature of the funds and the changing economy in general.

This article by me was originally published in Business Standard January 17, 2015

Share your experiences on how to manage child education expenses in the comments section below.

Manikaran Singal is the founder and Chief financial planner at Good Moneying Financial Solutions. He is a CERTIFIED FINANCIAL PLANNER CM and SEBI registered Investment adviser (Regd no. INA 100001620). He’s having 20+ years of experience in financial services space.

Manikaran Singal is the founder and Chief financial planner at Good Moneying Financial Solutions. He is a CERTIFIED FINANCIAL PLANNER CM and SEBI registered Investment adviser (Regd no. INA 100001620). He’s having 20+ years of experience in financial services space.")

{kind=link}

Nice article. I think this is one of the biggest priority as parent we have to think first. The cost education has rise unexpectedly and it will. I think the best way to achieve this target is long term ELSS/MF + Pure Term plan. If someone has opportunity then investing in property is also a good option.

Thanks Santanu. I would say whatever you do, just be aware of the results and pros and cons of the same. Don’t invest with closed eyes or wrong assumptions. One should be aware of the illiquid nature of property, volatile nature of equity and taxability/low returns of debt products. Plan and structure your requirements so it gets managed comfortably.

Equity for a 5-8 year horizon??? No way. Please clarify.

Kiran, Its equity oriented hybrid for 5,6,7 years and pure equity for 8 years. Moreover the idea of this article is to make you aware about the laddering approach. What to be included in the ladder purely depends on your risk tolerance.

Good blog again. Thanks for replying my previous questions. Please try to answer this question too. I have two SIP’s continuing from more than 2 yrs in large cap funds exclusively for my 2 kids aged 1 and 6 yrs respectively for their education and marriage which is more than 10 yrs from now.

My plan is simple to have 1 fund for each of the kid for both education and marriage, cos I don’t want to have too many funds to mess up. My approach would be to keep on investing in the sip’s and once the goal is nearer (first priority will be education) the approximate required corpus will be moved to fixed income funds, so that the corpus will be protected for education goal and also the sip will be keep on continuing for the other goal(marriage). Is my approach makes sense to you? please comment

Very Much. All the best Satish!!

my daughter 3 age and son 6 months baby i am planning education and marriage plan i invest one time lum amount payment 1 lakhs for 20 yrs term maturity amt .who invest MF,LIC or etc which better plan ?

Feroz, what i understand from your query is that you want to invest Rs 1 lakh for your children education and marriage, and you are confused between MF and LIC…right?

See, my view is to have insurance and investments separate. Buy Life insurance to cover your finanial responsibilities by buying adequate insurance cover and then invest the money in Mutual funds or other instruments which you feel comfortable with. Equity Mutual funds definitely gives good return in long term but it also is very volatile option in short term. Invest in a properly allocated plan and divide investments in different asset classes.

I think Sukanya Samriddhi Account will play a big role to manage girl child education and marriage expense in coming days.

Yes santanu, but i think the main drawback in that product is the taxability of returns and clubbing of income. In comparison to PPF i think SSA stands no where. Still it might suit some people depending on their requirements. Lets see where we can fit it into.